Generative AI could in principle feature a great diversity of sources in output responding to news-related queries.

But do various generative AI products actually do this?

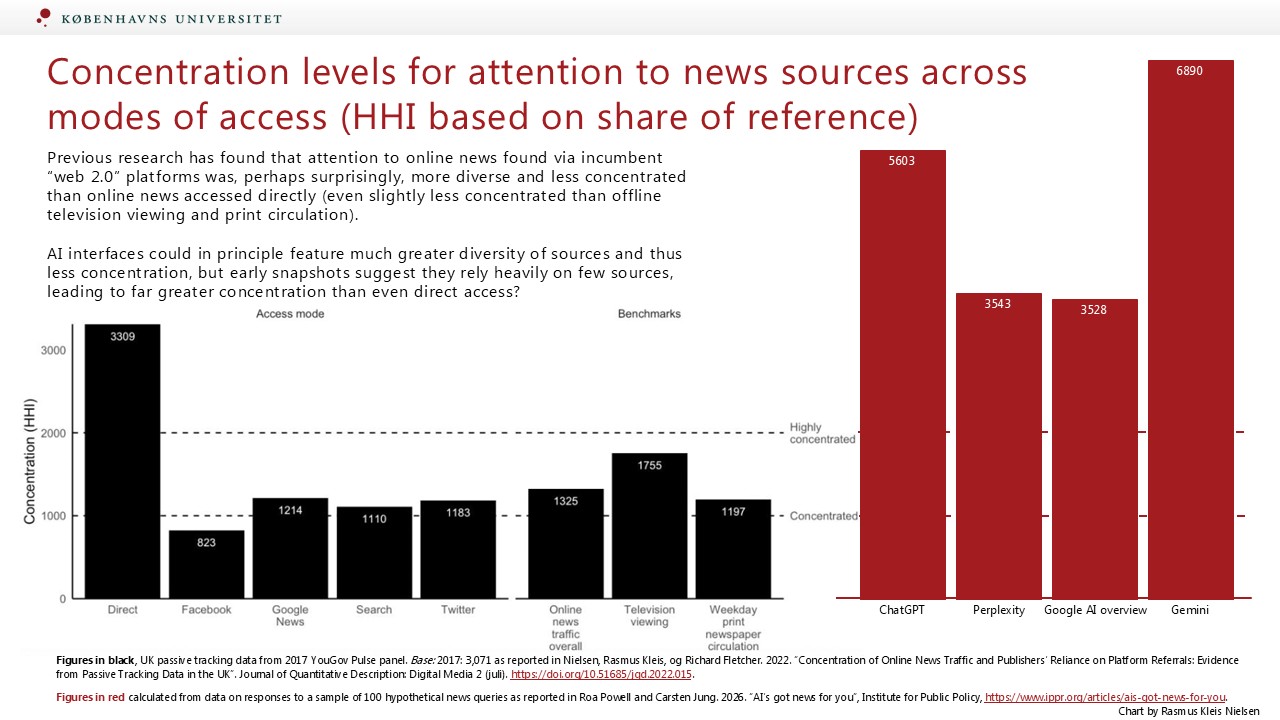

In early 2026, Roa Powell and Carsten Jung published a piece of research for the Institute for Public Policy suggesting maybe not – based on analysis of responses to a sample of 100 hypothetical UK news queries submitted to four different AI tools (ChatGPT, Perplexity, Gemini, and Google AI overview), they found that these tools draw “on a narrow range of prominent news brands”.

As a benchmark for interpreting their results, I have created the slide below.

The figures in red are my calculations of the Herfindahl–Hirschman Index (HHI) (a common measure of market concentration) for each of the four AI tools based on the share of reference that goes to each of the top ten news brands (as reported by Powell and Jung).

The figures in black are taken from this piece of work I did with Richard Fletcher included for comparison, namely similar HHI calculations based on historic data from the UK from 2017 for online news accessed directly, via search, news aggregators, or various kinds of social media, as well as, for further comparison, HHI figures for television viewing and weekly print newspaper circulation at the time.

The concentration of attention, with a few brands accounting for a very large share of reference, is far greater for the AI tools than any other form of access.

While the underlying data is not like-for-like comparison (the bulk of the 2017 data is based on passive tracking of actual UK users, the 2026 AI tool data is generated by prompting), I think the figures are still interesting and thought-provoking. (And not necessarily unique to the UK – Nikos Smyrnaios and Olivier Koch has published a piece of work, based on a somewhat different methodology, suggesting results for France that are also about the 2,000 bar for a highly concentrated market.)

It’s not just that Powell and Jung are right to stress that a narrow range of prominent news brands (some of whom have commercial deals with the AI companies) loom very large in AI output.

It is also that the concentration in question, measured here in terms of share of reference, is far, far greater than any of the different kinds of access we analyzed based on the 2017 data – even more concentrated than direct access, which itself was significantly more concentrated than any other kind of access at the time.

It also seems the (comparatively fewer) referrals they do drive are highly concentrated amongst a select few publishers, much more so than has been the case for search, social, or news aggregators.

(Underneath the topline, there is some diversity from tool to tool (just as we found different outlets doing well via different platforms), as Powell and Jung writes, their findings suggest “each AI tool prioritizing news brands in different ways, in each case foregrounding a distinct selection of news outlets compared with those that are currently most popular across the UK” – go read their report for more details.)

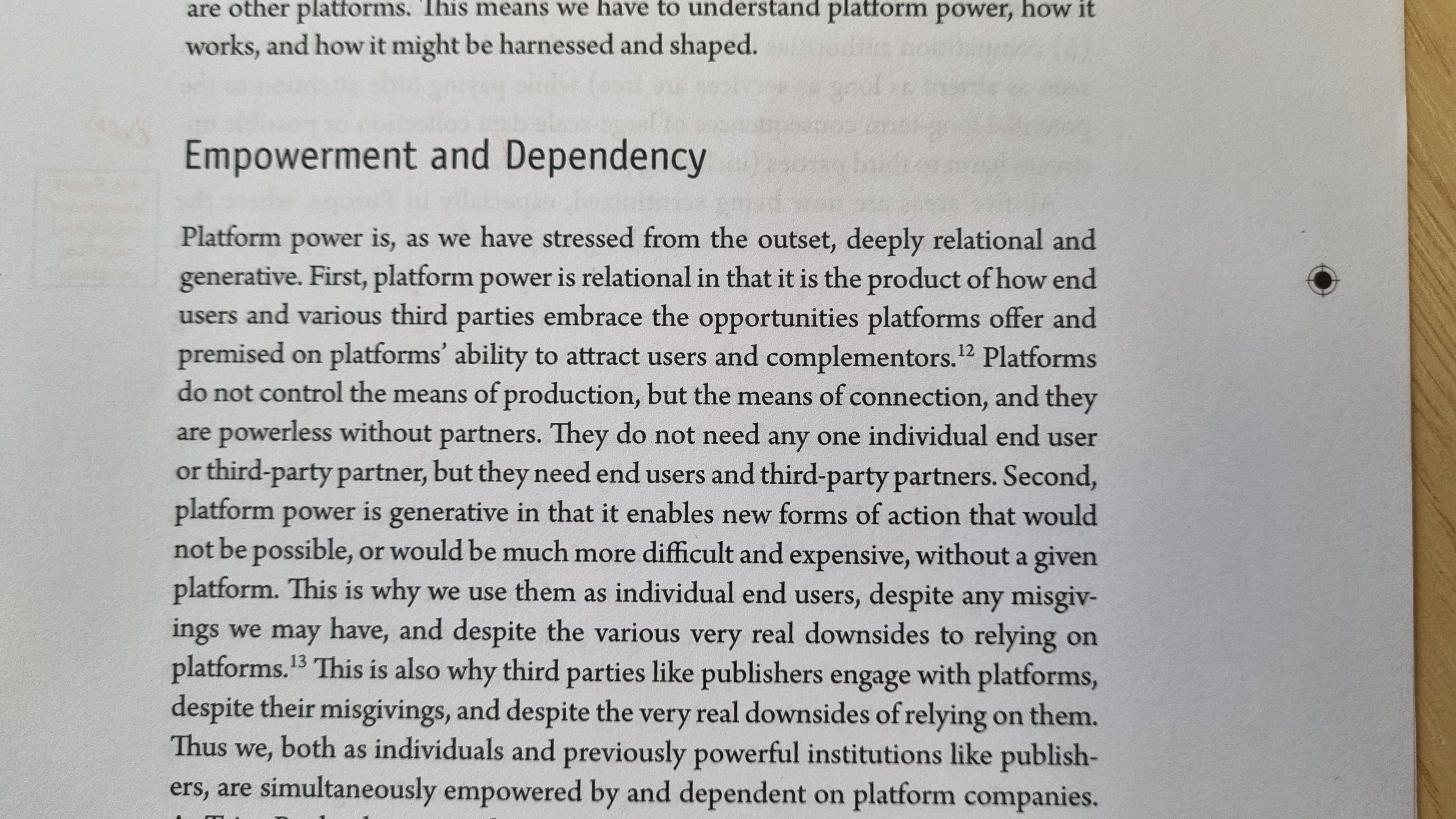

Our core argument is that the power of platforms is deeply relational and based on ability to attract end users and partners like publishers.

It’s always hard to summarize extensive empirical work briefly, but here a few key points from my short Twitter thread on the book, with a few pics of some central passages in the book.

Platforms do not control the means of production, but the means of connection, and they are powerless without partners. To understand their power we need to understand both reservations partners have and why they often embrace platforms nonetheless, continue to work with them.

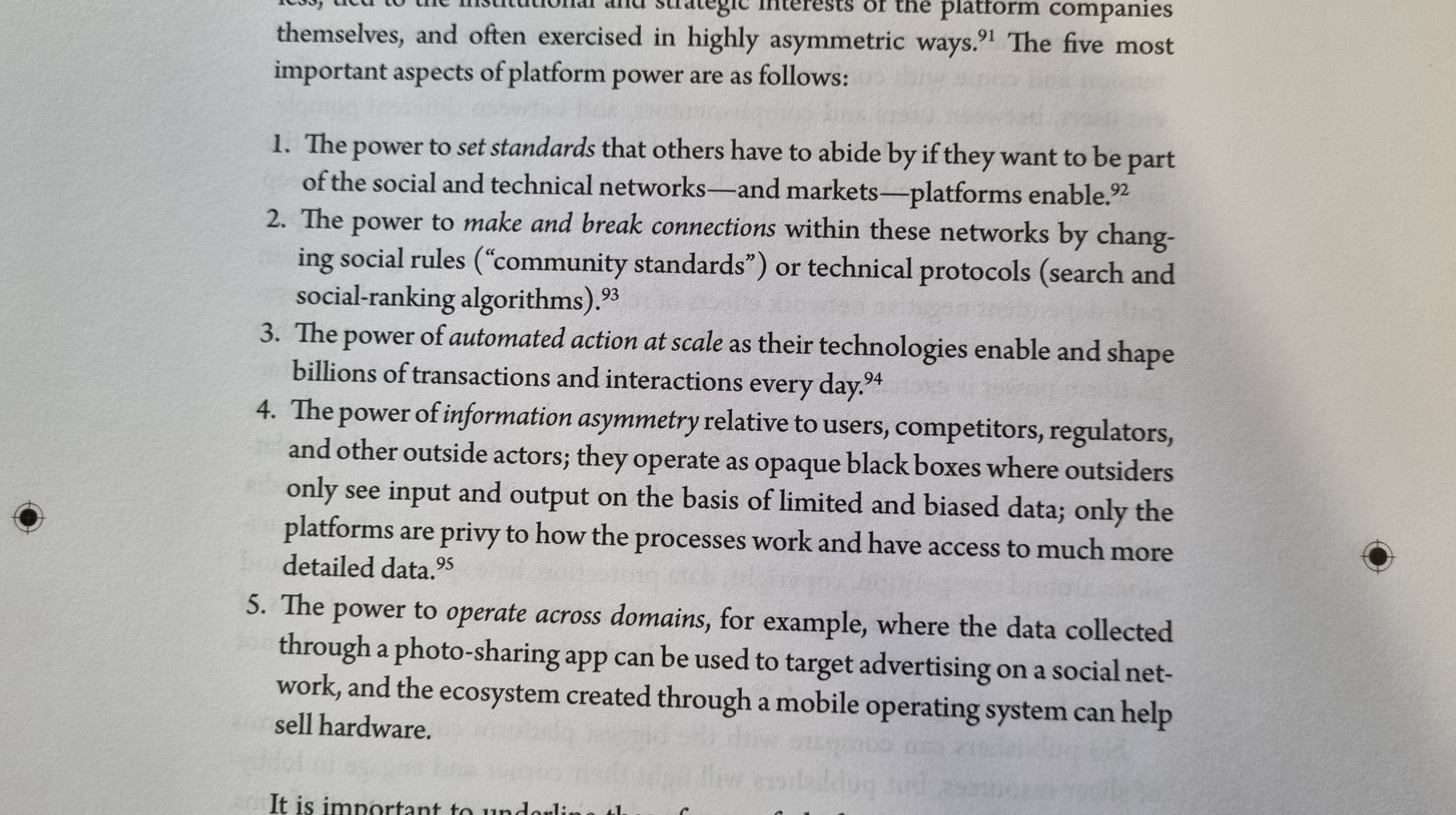

Platform power is an enabling, transformative, and productive form of power—and power nonetheless, tied to institutional and strategic interests of platform companies, often exercised in highly asymmetric ways.

It goes beyond hard and soft power. We identify five main aspects.

In the short run, actors make choices, in the long run, these choices become structures. Both platforms and partners have agency here, but there is a huge asymmetry between the biggest platforms (facing a few big platform rivals) and a multitude of much smaller publishers.

We approach platform power through an institutionalist lens, and focus on how it is exercised in relational ways through socio-technical systems that develop path-dependency and momentum over time and retain an imprint of their founding logics that shape ongoing interactions.

Our analysis is based on interviews across several countries, observation, background conversations, as well as on-the-record sources and more. In the methods appendix we reflect on individual and institutional positionality, including differences between the Reuters Institute for the Study of Journalism where I work and much of the research was done, and Simon Fraser University where Sarah now works.

The evolving relationships between platforms and publishers speaks to fundamental feature of the contemporary world – that not only individual citizens, but also social and political institutions, are becoming empowered by and dependent on a few private, for-profit companies

Very proud of the advance praise from colleagues with experiencing working in publishing companies, for platforms, as well as some leading academics researching digital media, including from Vivian Schiller, Nick Couldry, and José van Dijck. It means a lot to me personally to read what they kindly had to say about the book in advance of publication!

The research for this book was made possible by the prize money from the 2014 Tietgen Award, which funded Sarah’s position as a postdoctoral research fellow at the Reuters Institute for the Study of Journalism and the associated research costs.

We would like to thank first of all our interviewees and everybody else who has talked to us, joined off-the-record discussions we hosted, invited us to events, and let us sit in on meetings. The book would not have been possible without them sharing their perspectives, and whether they agree with our analysis or not, we hope they recognize the processes they are part of in what we write about here.

In addition, many different colleagues and friends have provided generous (and often challenging!) feedback as we worked on this, including David Levy, the former Director of the Reuters Institute for the Study of Journalism, and our many good colleagues there. Special thanks go to Chris Anderson, Gina Neff, Joy Jenkins, and Lucas Graves, who went through an entire draft manuscript with us and provided invaluable input. Daniel Kreiss and the anonymous reviewer helped further sharpen our thinking, and the series editor Andrew Chadwick went above and beyond in helping us develop our ideas. Fay Clarke, Felix Simon, and Gemma Walsh all did an outstanding job as research assistants at various stages of the project. Angela Chnapko at Oxford University Press masterfully guided us through the publication process.

My presentation notes for opening part of OECD panel on “Competition, Media and Digital Platforms” at the 2022 Open Competition day. Video of whole session here. More context at the end of the post.

News media used to operate in a low-choice environment where they had high market power over both audiences and advertisers.

Before the move to a digital, mobile, and platform dominated media environment, news media used to control both the channels of distribution and bundled the content people accessed, and captured a significant share of both audience attention and advertising spending because of the positions they occupied.

As a consequence, in markets that were geographically differentiated due to how print and broadcast distribution works, a significant number of news media made quite a lot of money by dominating local markets and specific audience niches.

News media now operate in what is, for citizens, a high-choice environment when it comes to content, and have very limited market power over both audiences and advertisers.

In a digital, mobile, and platform-dominated media environment, platforms increasingly control the channels of distribution, news is unbundled and competes for attention with all sorts of other content, and news media capture a much smaller share of audience attention and, as a consequence, of advertising spending.

This is a much, much more competitive market, and one characterized by very strong winner-takes-most dynamics where a few winners are doing well but many titles, especially legacy but also new entrants, have a much harder time making money.

A few key datapoints illustrate this –

A rough estimate is that people spend something like twenty percent of the time they spend reading print reading news, and something like ten percent of the time they spent watching television watching news.

By contrast, in the countries where we have data, all news media combined account for something like three to four percent of the time that people spend with digital media.

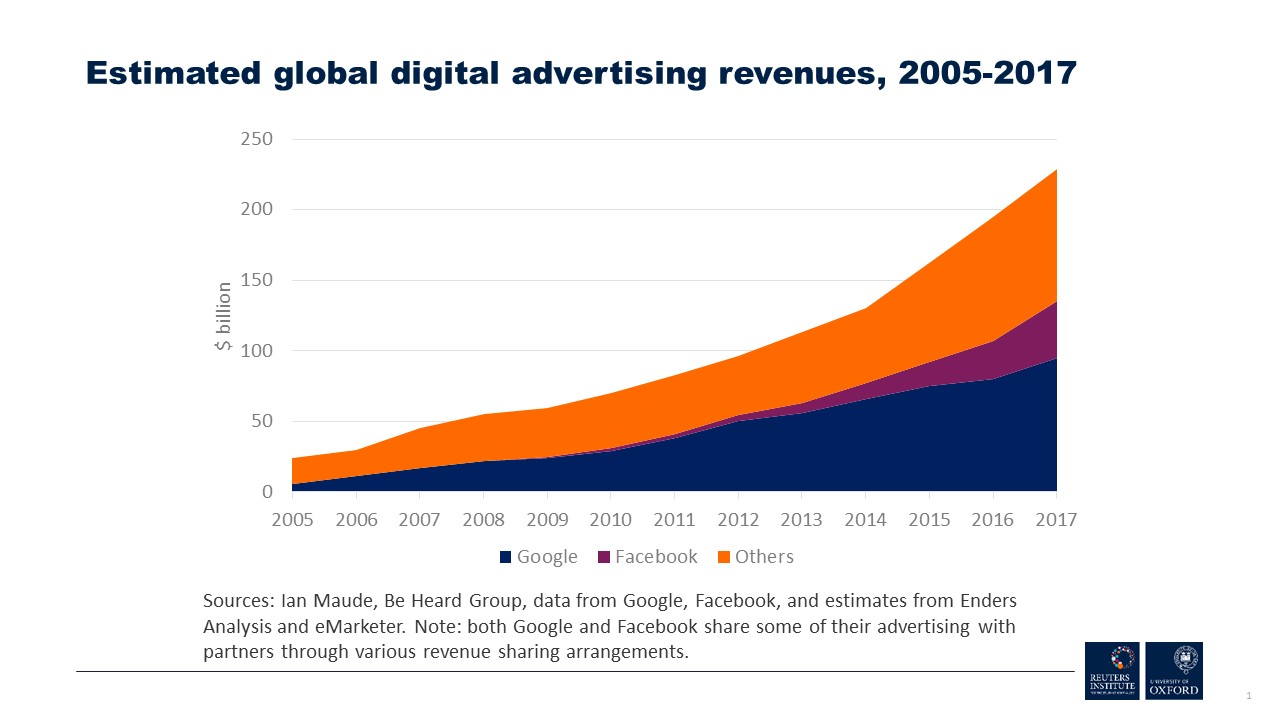

Since advertisers were never interested in the news per se, but in reaching audiences, it is not surprising that they have gone where the audience is.

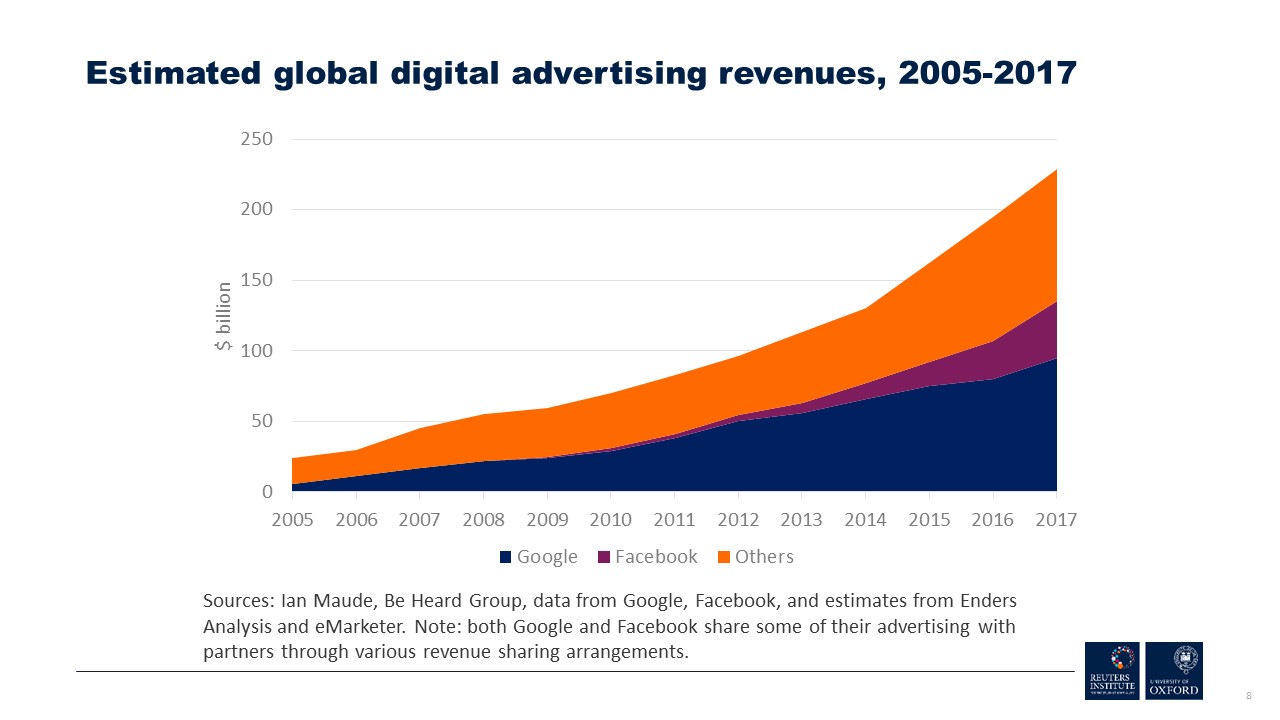

Online, that is, to a large extend, on platforms – and the popular success and evident market power of a few big platforms, most prominently Google and Facebook, has undoubtedly exacerbated the commercial challenges news media face as they account for a large share of total advertising sales.

The biggest platforms are the face of the challenge, but they are not all of it – it is important to recognize that, according to eMarketer, globally, most of the biggest sellers of digital advertising are platforms who can offer very low prices, very detailed targeting, and often both depth and breadth in terms of audience reach.

Advertisers still spend some money with news media, especially those news media who can offer premium brands and an advertising environment that stands out from just “stuff on the internet”. But over time I’d expect the share of advertising spending that goes to news media won’t be much higher than the share of audience attention that goes to news media – and, as said, right now, that’s a few percent.

If we look at those few percent of attention, and the news media industry specifically, we can see that the shift from a pre-digital to a digital environment has further intensified existing winner-takes-most dynamics.

In the past, economies of scale and high barriers to entry drove consolidation and the formation of local monopolies and oligopolies. Media markets have always been highly concentrated.

In a digital environment where geography no longer presents a meaningful barrier to entry, the same dynamics are playing out at a national level and to a smaller extend at a global level.

Look at attention, and by extension advertising, first.

In the markets where we have data, out of hundreds of competing news media, typically, a handful of titles – almost always national brands – account for half or more of all time spent with news online.

That’s the big head – at the long-tail end of the distribution, in the US, all local news titles combined have been estimated to account for less than one-sixth of all time spend with news online, in the UK, about one-tenth.

It stands to reason that a tiny amount of attention combined with no market power over audiences or advertisers is less lucrative than being the dominant player in local content and local advertising.

Look at paying for news next.

Here too we see strong winner-takes-most dynamics. In the markets where we have data, again, a small number of predominantly national titles, out of hundreds of news media, often account for half or more of all digital news subscriptions.

They are the big head – at the long-tail end of the distribution, with some important exceptions, local titles have seen limited growth in digital subscriptions.

Where does this leave us?

It leaves us in a place where I think we should expect top-line revenues in the news industry as a whole to continue to decline for some time, driven primarily by audience and advertiser choices, and compounded by the success of platforms, as relatively lucrative legacy print and broadcast operations continue their long-term structural decline (print, traditional TV) or at best stagnate (which I consider best case scenario for linear scheduled TV) and digital is a much more challenging and competitive market.

And it points to a future where existing winner-takes-most dynamics in the business of news, for both attention, advertising, and reader revenues, are reinforced.

It will probably be a smaller industry than news was in the 1990s – but with a few percent of total advertising expenditures, a growing number of digital subscribers served at near-zero marginal costs, and auxiliary revenues from ecommerce and the like it will still be a multi-billion dollar industry, and one that will probably invest a greater share of revenues in editorial than it ever did, because the very high distribution and production costs associated with offline are falling away.

Compared to the recent past, it will be characterized by few winners – dominant national titles, and those new entrants who make good use of the gift of digital distribution at low cost, keep their content distinct and their costs low, and manage platform risk well.

And there will be many losers – especially among also-ran national titles, local titles stuck with a pre-digital cost structure, as well as titles trying to build a sustainable business around serving less privileged and often historically underserved parts of the public (as well as all titles with owners who prefer short-term asset stripping over the uncertain returns on long-term investment in digital transformation).

It’s going to be amazing for people like me, the most lucrative affluent, highly educated, news loving part of the public. It’s looking a lot more mixed for the majority of the public. The latter point is potentially problematic if one believes, as I personally do, that independent professional journalism, with its imperfections, play an important role in our societies, but that is more a political question.

As part of the opening, I was given four minutes to say a few things about the following questions: “How has news media changed in the digital age? Changes in the revenue model and changes in consumer behaviour? Any difference between large and small/local outlets?”

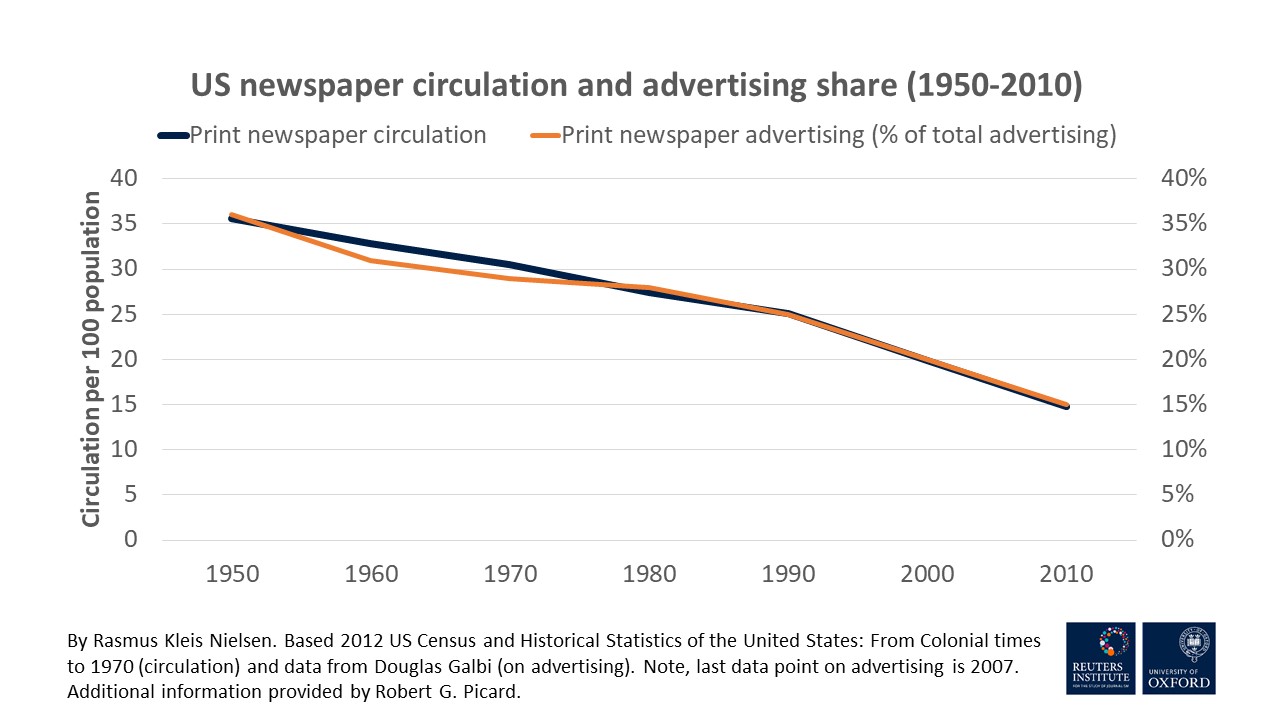

This post contains my presentation notes – a lot of ground to cover in four minutes! They draw on this handbook chapter from 2020, which I still hope is useful in capturing the main dynamics as I see them. I’ve added a few links to underlying evidence and two charts taken from the handbook chapter.

Two addendums to the notes above. First, as I made clear in the panel discussion, OECD member countries are very different, and so is the business of news (and political context) from case to case, this is just an attempt to capture what I see as the high level trends. Second, in the panel I somehow came to be cast as the pessimist – that’s not how I personally think of my analysis. While sobering, I think it also gives ground for evidence-based optimism. Whether you find it optimistic, pessimistic, or realistic, I give it in the spirit of James Baldwin’s piercing line: “Not everything that is faced can be changed; but nothing can be changed until it is faced”, hence the title of this post.

(Oh, and finally, I wonder how many other presenters at OECD events are caught red-handed on video with a half-dozen Foucault books on the shelf behind them!)

When people get news via search engines, social media, and others forms of distributed discovery — rather than going directly to a website or app — they often cannot correctly recall what brand e a story they have read actually came from.

In a new article in New Media & Society led by Antonis Kalogeropoulos and with Richard Fletcher, we’ve looked more closely at the factors that influence correct news brand attribution in different environments.

The digital media environment is increasingly characterized by distributed discovery, where media users find content produced by news media via platforms like search engines and social media. Here, we measure whether online news users correctly attribute stories they have accessed to the brands that have produced them. We call this “news brand attribution.” Based on a unique combination of passive tracking followed by surveys served to a panel of users after they had accessed news by identifiable means (direct, search, social) and controlling for demographic and media consumption variables, we find that users are far more likely to correctly attribute a story to a news brand if they accessed it directly rather than via search or social. We discuss the implications of our findings for the business of journalism, for our understanding of source cues in an increasingly distributed media environment and the potential of the novel research design developed.

Back in June, Journalism: Theory, Practice, Critique published an article based on the ongoing, comparative qualitative research Alessio Cornia, Annika Sehl, and I have been doing on how European news media are adapting to digital.

Based on interviews as 12 different private sector legacy news media, we show how many are rethinking the traditional separation of editorial and commercial operations, and that the increasing integration between editorial and commercial (not assimilation of editorial into commercial, not hierarchical relegation of editorial to commercial) is motivated by the same aspiration as the traditional separation: to ensure professional autonomy, only today that is pursued by working with other parts of the organization to jointly ensure commercial sustainability, rather than by trying to remain completely separate from commercial issues..

The separation between editorial and business activities of news organisations has long been a fundamental norm of journalism. Journalists have traditionally considered this separation as both an ethical principle and an organisational solution to preserve their professional autonomy and isolate their newsrooms from profit-driven pressures exerted by advertising, sales and marketing departments. However, many news organisations are increasingly integrating their editorial and commercial operations. Based on 41 interviews conducted at 12 newspapers and commercial broadcasters in six European countries, we analyse how editors and business managers describe the changing relationship between their departments. Drawing on previous research on journalistic norms and change, we focus on how interviewees use rhetorical discourses and normative statements to de-construct traditional norms, build new professionally accepted norms and legitimise new working practices. We find, first, that the traditional norm of separation no longer plays the central role that it used to. Both editors and managers are working to foster a cultural change that is seen as a prerequisite for organisational adaptation to an increasingly challenging environment. Second, we find that a new norm of integration, based on the values of collaboration, adaptation and business thinking, has emerged. Third, we show how the interplay between declining and emerging norms involves a difficult negotiation. Whereas those committed to the traditional norm see commercial considerations as a threat to professional autonomy, our interviewees see the emerging norm as a new way of ensuring professional autonomy by working with other parts of the organisation to jointly ensure commercial sustainability.

Working with RISJ colleagues Tim Libert (now at Carnegie Mellon) and Lucas Graves, I’ve worked on a short piece of research examining changes in third-party content and cookies on news sites across seven EU countries before and after GDPR.

Tim led the work using his tool webXray to collect and analyse a total of 10,168 page loads, nearly 1 million content requests, and 2.7 million cookies from April (pre-GDPR) and July (post-GDPR) across over 200 news sites.

We find that news sites continue to be deeply intertwined with a wide range of third parties, especially in advertising, social media, and the like, though there is some drop in the amount of third party content and cookies after GDPR.

This factsheet compares the prevalence of third-party web content and cookies on a selection of European news websites one month before and one month after the introduction of the EU General Data Protection Regulation (GDPR). To understand how news organisations may be adapting to the new privacy framework, prominent news websites in seven countries (Finland, France, Germany, Italy, Poland, Spain, and the UK) were analysed during the months of April and again in July 2018.

While there is no change in the overall percentage of pages from news providers which contain some form of third-party content (99%) or third-party cookies (98%), we find a 22% drop in the number of cookies set without user consent and an observable decrease in third-party social media content.

Here is a a PDF of my draft chapter on “The Changing Economic Contexts of Journalism” for the 2nd edition of the ICA Handbook of Journalism Studies, edited by Karin Wahl-Jorgensen and Thomas Hanitzsch.

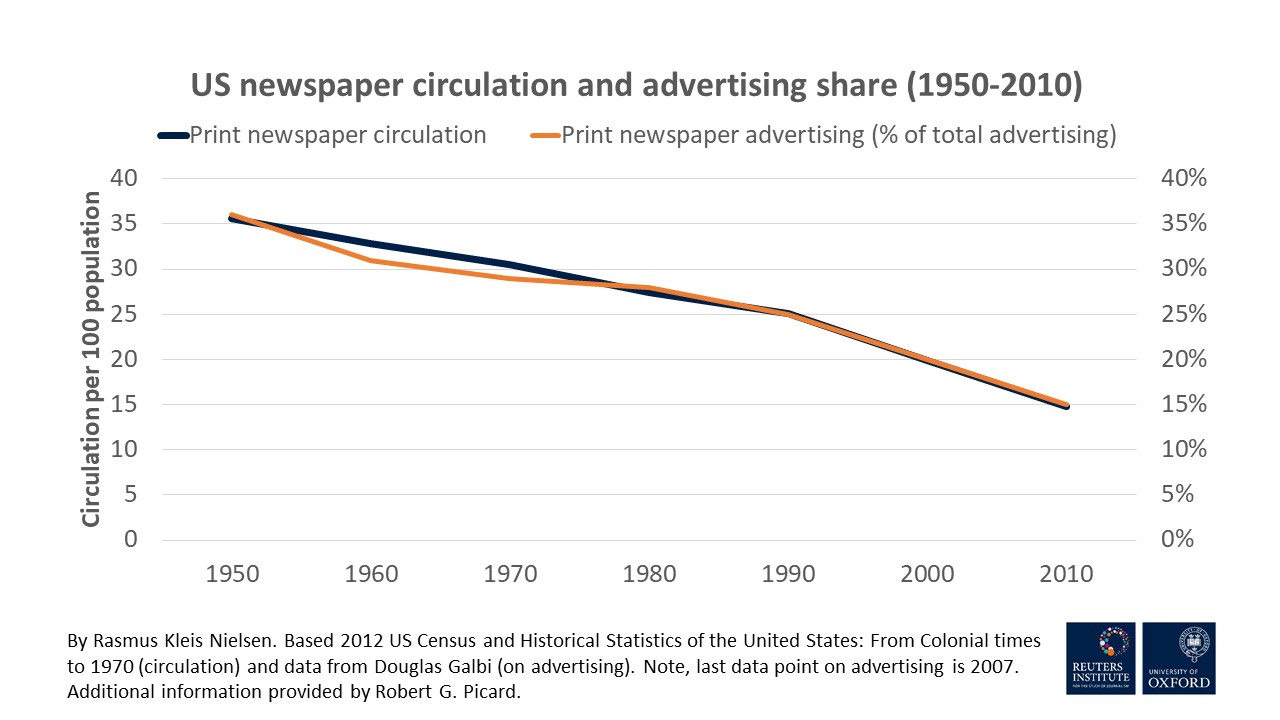

I’ve tried to summarize in about 30 pages the most important basic features of the business of news, its historical evolution (like the graph below), and where it is heading.

I’ve got a few weeks to finish it – suggestions welcome! (It is far too long, so suggestions of cuts especially welcome.)

I hope the chapter will provide a useful and readable introduction for both journalists and journalism studies students/scholars to key concept like the attention economy, two-sided markets, high fixed cost/low variable cost, news as a non-rivalrous experience good, market failure, media capture, and what the move to digital does and does not change.

Please note, I’ve prioritized media economics, historical background, and key current changes. Can’t cover everything in one chapter. Day-to-day developments are better covered in trade publications. And there is much, much more research out there (though too little I know of from the Global South), by economists, and by others. For those interested in critical political economy, I recommend the work of fx Robin Mansell and Janet Wasko, for those interested in ownership, the immense empirical research efforts lead by Eli Noam, Vanita Kohli-Khandekar’s work on the Indian media business has been really useful for me in other work, for those interested in advertising, the work of for example Joe Turow, and much more beyond that.

Here are my background notes for the session, in part based on things I’ve written elsewhere, including this Nieman Lab post about how the business of news after advertising may look a lot like the business of news before advertising (more elite-oriented, more often based on subsidies from for example political patrons) and this longer book chapter.

Key points are–

News production has historically been funded by advertising and sales, but the advertising investment in news is in long-term structural decline—in the US, for example, newspapers’ share of total advertising has been in steady decline for more than half a century.

This is really important, because newspapers still account for the majority of the funds invested in news production. In US, Bureau of Labor statistics suggest print publishers still accounted for more than half of all journalists employed as of 2016.

Most legacy news media will never make kind of money off news that they made in past, because

1) they no longer have market power they had in low-choice environment,

2) their content bundle is being unbundled, and

3) they compete head-to-head w/platforms that offer advertisers cheap, targeted, unduplicated reach, and therefore dominate digital advertising.

(Some of this is shared with various partners through revenue sharing and the like — Google, for example, reported that they paid out 24% of total advertising revenues in Q4 2017 in various forms of “traffic acquisition costs”.)

So, given dwindling cross-subsidies from legacy ops like print/broadcast, what lies ahead, beyond cost-cutting in many news orgs, in some countries possibly public subsidies, and in more and more cases a return to various forms of politically-motivated investment in news?

My fellow panellists demonstrate different approaches.

At Gizmodo, Raju Narisetti has pursued diversification with emphasis on different kinds of advertising.

At the Financial Times, Renee Kaplan and her colleagues focus on reader revenues.

At Buzzfeed, Janine Gibson and her colleagues have pursued off-site reach and revenue-sharing with platforms.

(Beyond this, we can look at the incremental growth in non-profit models for news provision, though the resources in aggregate are far smaller than those generated by private sector, for-profit news media.)

There is no one model that is right for every publisher in every country, but the basic structural change seem clear and near-universal — advertising remains an impotant part of the business of news, but traditional forms of advertising (print, broadcast, and digital display) are declining, because most advertisers seem to think they get more value for money elsewhere (and they were always interested in audiences’ attention, not news in itself).

News organizations who want to thrive in this changing environment have to operate very lean cost structures and seek to generate other revenues, for example by pursuing new forms of distinct digital advertising, by seeking reader revenues, or by trying to leverage platforms for reach and revenue-sharing.

Back in 2010, David Levy and I edited a collection of essays on The Changing Business of Journalism and its Implications for Democracy, published by the Reuters Institute for the Study of Journalism here in Oxford.

We have today made the whole book available for download here [PDF]. (All the hard copies have been sold!)

In addition to the chapters written by David, Robert Picard, and myself, the book contains interesting contributions by Alice Antheaume (Sciences Po, Paris), Michael Brüggemann (University of Zürich, now Hamburg), Frank Esser (University of Zürich), John Lloyd (University of Oxford/Financial Times), Hannu Nieminen (University of Helsinki), Mauro Porto (Tulane University), Michael Schudson (Columbia University), Daya Kishan Thussu (University of Westminster), and Sacha Wunsch-Vincent (World Intellectual Property Organisation and formerly OECD).

The Changing Business of Journalism and its Implications for Democracy, as the only rigorous global survey of a situation usually discussed on the basis of anecdote and unproved assertion, is an indispensable and necessary work. It ought to open the way for real progress in reinventing journalism.

Nicholas Lemann, Dean and Henry R. Luce Professor at the Columbia University Graduate School of Journalism

This is a very detailed and rich analysis of the structural changes in today’s business of journalism: the media in many countries face a deep crisis caused both by new technologies and more general economic circumstances while in others they are experiencing rapid growth. In both cases the entire structure of the field is undergoing a dramatic change in terms of professional practice and in how media are organized and run. This book represents an indispensable tool for all those who want to understand where journalism and democracy are going today.

Paolo Mancini, Professor at Università di Perugia and co-author of Comparing Media Systems (Cambridge, 2004).

The full table of content looks as follows:

Contents

Executive summary

1. The Changing Business of Journalism and its

Implications for Democracy

Rasmus Kleis Nielsen and David A. L. Levy

2. A Business Perspective on Challenges Facing Journalism

Robert G. Picard

3. Online News: Recent Developments, New Business

Models and Future Prospects

Sacha Wunsch-Vincent

4. The Strategic Crisis of German Newspapers

Frank Esser and Michael Brüggemann

5. The Unravelling Finnish Media Policy Consensus?

Hannu Nieminen

6. The French Press and its Enduring Institutional Crisis

Alice Antheaume

7. The Press We Destroy

John Lloyd

8. News in Crisis in the United States: Panic – And Beyond

Michael Schudson

9. The Changing Landscape of Brazil’s News Media

Mauro P. Porto

10. The Business of ‘Bollywoodized’ Journalism

Daya Kishan Thussu

11. Which Way for the Business of Journalism?

Rasmus Kleis Nielsen and David A. L. Levy

March 1, I spoke at a workshop on the future of news in the European Parliament organized by MEP Marietje Schaake (Dutch Democratic Party (D66),part of the Alliance of Liberals and Democrats for Europe (ALDE) group).

The video should be well worth watching — lots of interesting and important discussion, of fake news, of filter bubbles, and of various policy issues including copyright.

I was particularly struck by the contrast between what I couldn’t help but feel was deep pessimism from Francois Le Hodey (CEO of the IPM publishing group which owns, amongst other things, the daily newspaper La Libre Belgique) and Rob Wijnberg (co-founder and editor of DeCorrespondent), who had a more optimistic take.

Despite (rightly) highlighting that many European publishers have built significant digital audiences and are investing aggressively in digital initiatives, Le Hodey said several times “we have got five years”. He argued that it takes “between €50 million and €200 million” a year to fund and run a proper newsroom, and pointed out that print revenues are currently shrinking much faster than digital revenues are growing.

Wijnberg in a way was much more critical of existing journalism in terms of the quality and public value of much of it (arguing it often doesn’t actually help people understand the world, because it focuses on episodes and exceptions rather than longer-term developments and general trends). But he was also much more optimistic about developing a sustainable business around reader contributions and others sources — as deCorrespondent has done in the Netherlands, now with more than 50,000 paying subscribers. His optimism may in part be about expectations — unlike the figure Le Hodey offered (based on what newspapers have historically been able to invest), he said deCorrespondent operates on a budget around €3 million a year — not easy to generate (as other start-ups have found), but surely easier than €50+ million. His position has, I felt, a lot in common with that Melissa Bell outlined earlier this year in her lecture at Oxford.

I gave a short presentation based on some of our recent research, including our work on private sector legacy news media (this report, with Alessio Cornia and Annika Sehl), digital-born news media (this report with Tom Nicholls and Nabeelah Shabbir), and broader trends in media use, markets, and policy across Europe (this report with Alessio Cornia and Antonis Kalogeropoulos), as well as some of the work we have under way on the notion of filter bubbles (see a short piece Richard Fletcher and I wrote here).

My main points are summarized on the slide below.

The other speakers were Francois Le Hodey (CEO, IPM Group), Rob Wijnberg (Founder, De Correspondent), Marco Pancini (Director Of EU Public Policy, Google), Anne Appelbaum (Columnist, Washington Post), Richard Allen (Vice President Public Policy EMEA, Facebook), and Krisztina Stump (Deputy Head of Unit, Converging Media, Content Unit, Directorate General, Communications Networks, Content and Technology, European Commission).