My presentation notes for opening part of OECD panel on “Competition, Media and Digital Platforms” at the 2022 Open Competition day. Video of whole session here. More context at the end of the post.

News media used to operate in a low-choice environment where they had high market power over both audiences and advertisers.

Before the move to a digital, mobile, and platform dominated media environment, news media used to control both the channels of distribution and bundled the content people accessed, and captured a significant share of both audience attention and advertising spending because of the positions they occupied.

As a consequence, in markets that were geographically differentiated due to how print and broadcast distribution works, a significant number of news media made quite a lot of money by dominating local markets and specific audience niches.

News media now operate in what is, for citizens, a high-choice environment when it comes to content, and have very limited market power over both audiences and advertisers.

In a digital, mobile, and platform-dominated media environment, platforms increasingly control the channels of distribution, news is unbundled and competes for attention with all sorts of other content, and news media capture a much smaller share of audience attention and, as a consequence, of advertising spending.

This is a much, much more competitive market, and one characterized by very strong winner-takes-most dynamics where a few winners are doing well but many titles, especially legacy but also new entrants, have a much harder time making money.

A few key datapoints illustrate this –

A rough estimate is that people spend something like twenty percent of the time they spend reading print reading news, and something like ten percent of the time they spent watching television watching news.

By contrast, in the countries where we have data, all news media combined account for something like three to four percent of the time that people spend with digital media.

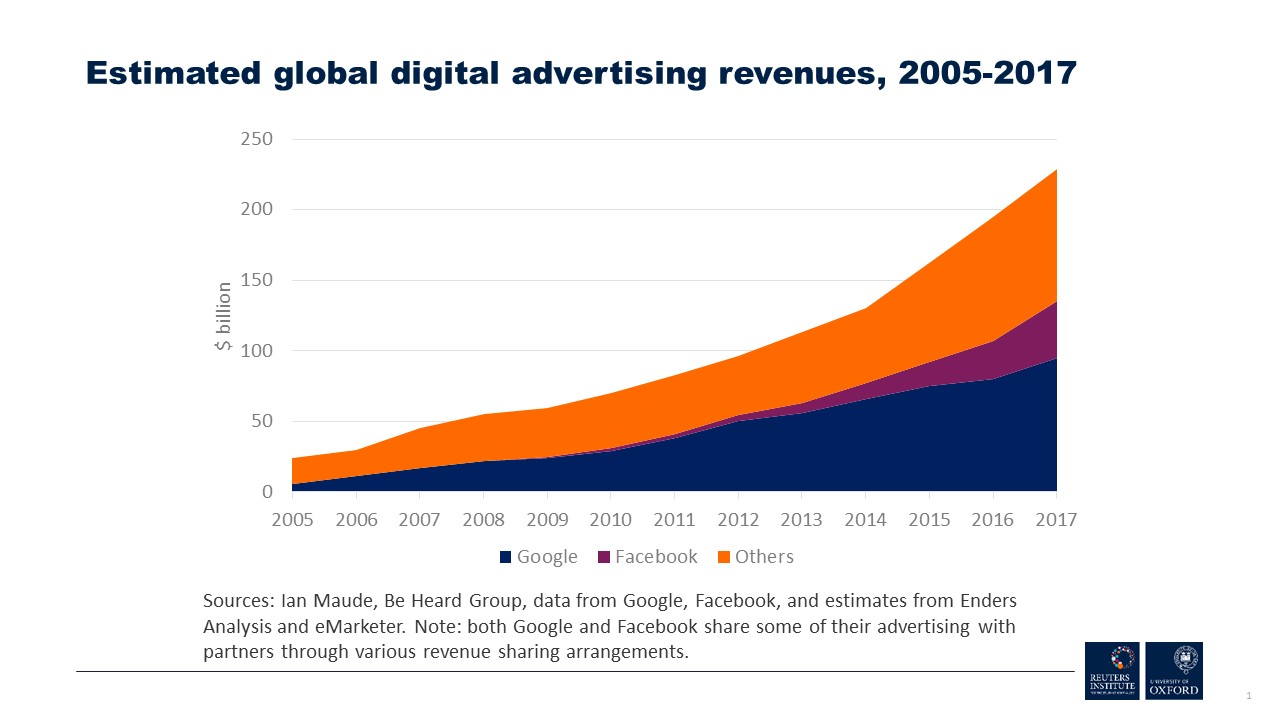

Since advertisers were never interested in the news per se, but in reaching audiences, it is not surprising that they have gone where the audience is.

Online, that is, to a large extend, on platforms – and the popular success and evident market power of a few big platforms, most prominently Google and Facebook, has undoubtedly exacerbated the commercial challenges news media face as they account for a large share of total advertising sales.

The biggest platforms are the face of the challenge, but they are not all of it – it is important to recognize that, according to eMarketer, globally, most of the biggest sellers of digital advertising are platforms who can offer very low prices, very detailed targeting, and often both depth and breadth in terms of audience reach.

Advertisers still spend some money with news media, especially those news media who can offer premium brands and an advertising environment that stands out from just “stuff on the internet”. But over time I’d expect the share of advertising spending that goes to news media won’t be much higher than the share of audience attention that goes to news media – and, as said, right now, that’s a few percent.

If we look at those few percent of attention, and the news media industry specifically, we can see that the shift from a pre-digital to a digital environment has further intensified existing winner-takes-most dynamics.

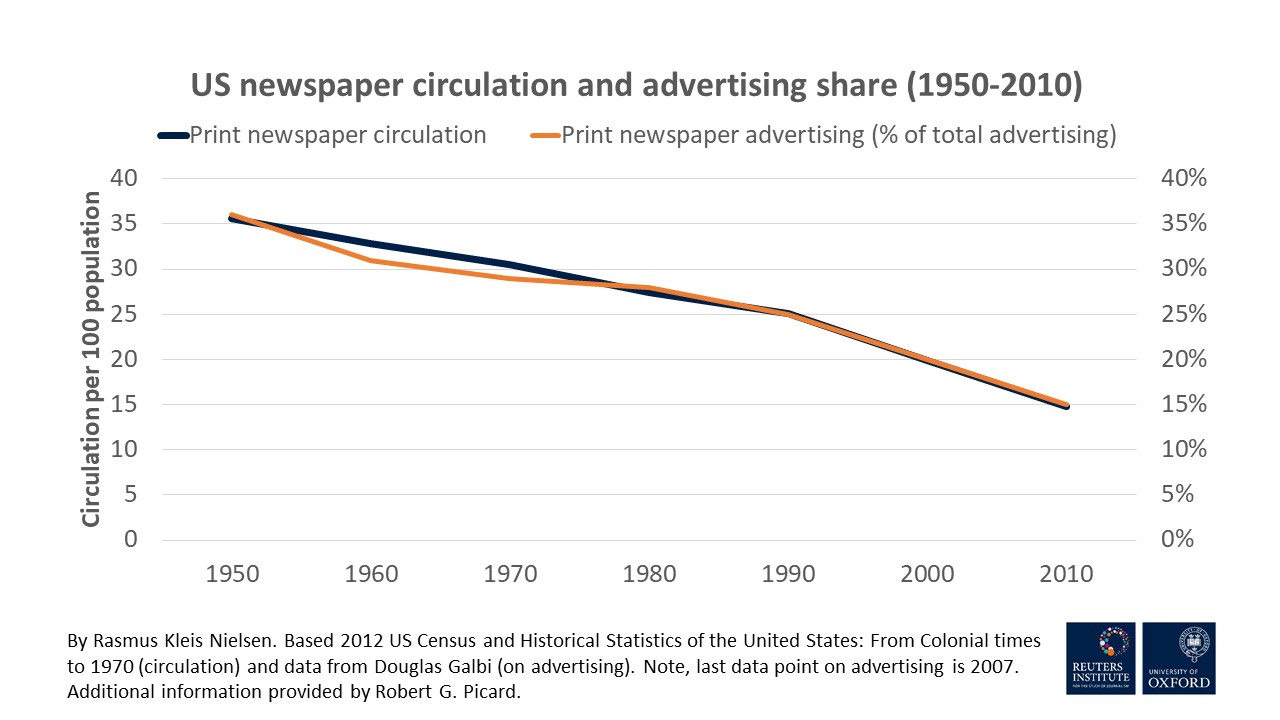

In the past, economies of scale and high barriers to entry drove consolidation and the formation of local monopolies and oligopolies. Media markets have always been highly concentrated.

In a digital environment where geography no longer presents a meaningful barrier to entry, the same dynamics are playing out at a national level and to a smaller extend at a global level.

Look at attention, and by extension advertising, first.

In the markets where we have data, out of hundreds of competing news media, typically, a handful of titles – almost always national brands – account for half or more of all time spent with news online.

That’s the big head – at the long-tail end of the distribution, in the US, all local news titles combined have been estimated to account for less than one-sixth of all time spend with news online, in the UK, about one-tenth.

It stands to reason that a tiny amount of attention combined with no market power over audiences or advertisers is less lucrative than being the dominant player in local content and local advertising.

Look at paying for news next.

Here too we see strong winner-takes-most dynamics. In the markets where we have data, again, a small number of predominantly national titles, out of hundreds of news media, often account for half or more of all digital news subscriptions.

They are the big head – at the long-tail end of the distribution, with some important exceptions, local titles have seen limited growth in digital subscriptions.

Where does this leave us?

It leaves us in a place where I think we should expect top-line revenues in the news industry as a whole to continue to decline for some time, driven primarily by audience and advertiser choices, and compounded by the success of platforms, as relatively lucrative legacy print and broadcast operations continue their long-term structural decline (print, traditional TV) or at best stagnate (which I consider best case scenario for linear scheduled TV) and digital is a much more challenging and competitive market.

And it points to a future where existing winner-takes-most dynamics in the business of news, for both attention, advertising, and reader revenues, are reinforced.

It will probably be a smaller industry than news was in the 1990s – but with a few percent of total advertising expenditures, a growing number of digital subscribers served at near-zero marginal costs, and auxiliary revenues from ecommerce and the like it will still be a multi-billion dollar industry, and one that will probably invest a greater share of revenues in editorial than it ever did, because the very high distribution and production costs associated with offline are falling away.

Compared to the recent past, it will be characterized by few winners – dominant national titles, and those new entrants who make good use of the gift of digital distribution at low cost, keep their content distinct and their costs low, and manage platform risk well.

And there will be many losers – especially among also-ran national titles, local titles stuck with a pre-digital cost structure, as well as titles trying to build a sustainable business around serving less privileged and often historically underserved parts of the public (as well as all titles with owners who prefer short-term asset stripping over the uncertain returns on long-term investment in digital transformation).

It’s going to be amazing for people like me, the most lucrative affluent, highly educated, news loving part of the public. It’s looking a lot more mixed for the majority of the public. The latter point is potentially problematic if one believes, as I personally do, that independent professional journalism, with its imperfections, play an important role in our societies, but that is more a political question.

The OECD invited me to join a panel on “Competition, Media and Digital Platforms” at the 2022 Competition Open day. A video of the panel, also featuring Professors Michel Gal, Martin Peitz, Miklos Sarvary and chaired by Matteo Giangaspero from the OECD, is here.

As part of the opening, I was given four minutes to say a few things about the following questions: “How has news media changed in the digital age? Changes in the revenue model and changes in consumer behaviour? Any difference between large and small/local outlets?”

This post contains my presentation notes – a lot of ground to cover in four minutes! They draw on this handbook chapter from 2020, which I still hope is useful in capturing the main dynamics as I see them. I’ve added a few links to underlying evidence and two charts taken from the handbook chapter.

Two addendums to the notes above. First, as I made clear in the panel discussion, OECD member countries are very different, and so is the business of news (and political context) from case to case, this is just an attempt to capture what I see as the high level trends. Second, in the panel I somehow came to be cast as the pessimist – that’s not how I personally think of my analysis. While sobering, I think it also gives ground for evidence-based optimism. Whether you find it optimistic, pessimistic, or realistic, I give it in the spirit of James Baldwin’s piercing line: “Not everything that is faced can be changed; but nothing can be changed until it is faced”, hence the title of this post.

(Oh, and finally, I wonder how many other presenters at OECD events are caught red-handed on video with a half-dozen Foucault books on the shelf behind them!)