The 2024 Reuters Institute Digital News Report is out, documenting scale and scope of ‘platform resets’ and much more. It is a team effort by lead author Nic Newman, Richard Fletcher, Craig Robertson, Amy Ross, and myself, working with our country partners. The report covers 47 market accounting for more than half of the world’s population, and is made possible by our 19 funders. A real pleasure to chair the panel discussion at the global launch at Reuters News this morning, featuring Rozina Breen (editor-in-chief, The Bureau of Investigative Journalism), Anna Bateson (CEO of the Guardian Media Group), Rachel Corp (CEO of ITN), and Matthew Keen (Head of Operations and Strategy, Reuters).

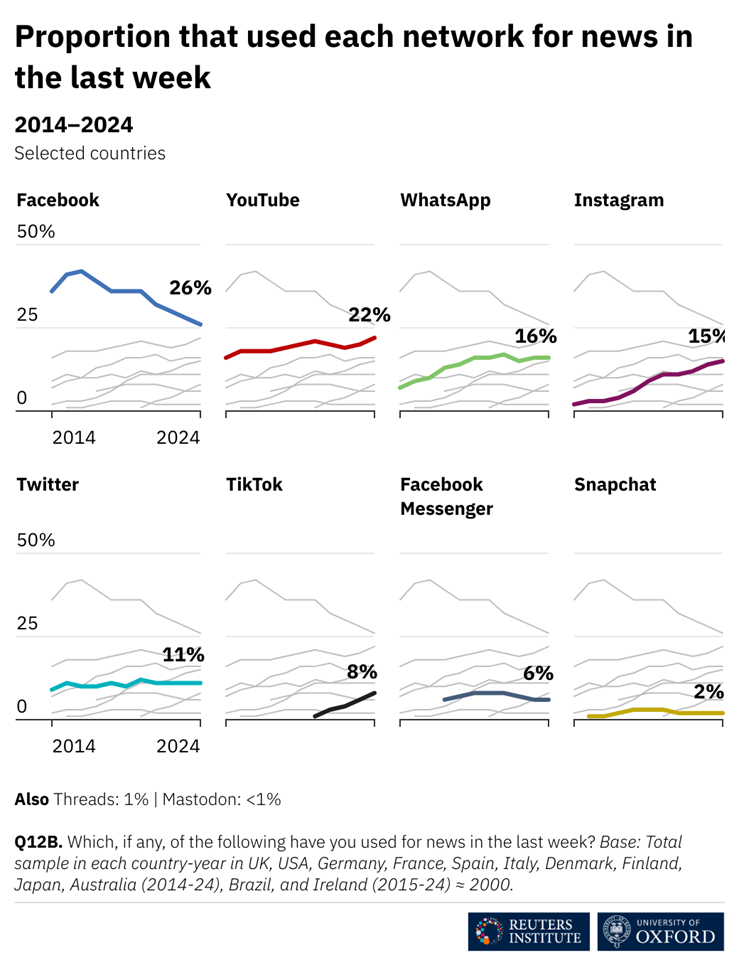

A key theme this year is how a series of ‘platform resets’ are shaping how people access news and changing the environment publishers operate in – even as the percentage who say they get news via Facebook continues to decline, a range of other social, video, and messaging platforms are growing in importance for discovery, many focused on on-site video, visuals, and more private experiences.

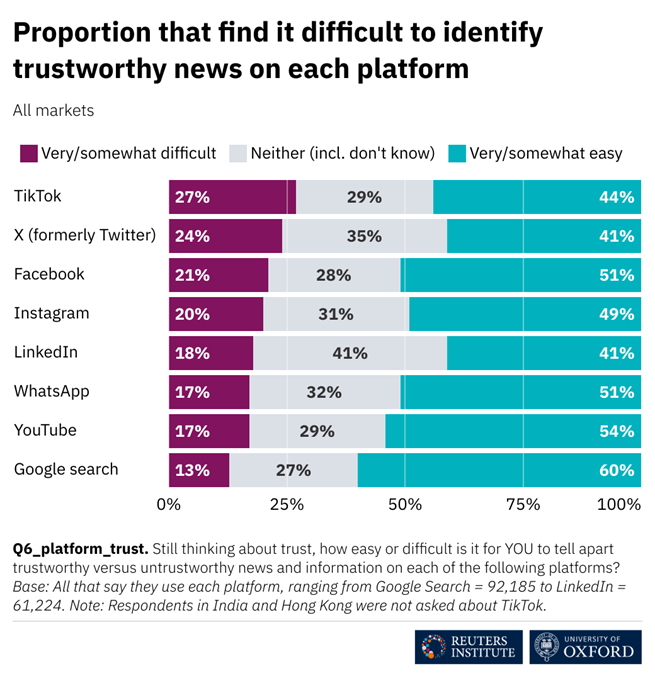

Generally, many of our respondents say they find it at least somewhat easy to tell trustworthy and untrustworthy news and information apart on various platforms, but there are real differences, with more people concerned about how to navigate information on e.g. TikTok, X, Facebook.

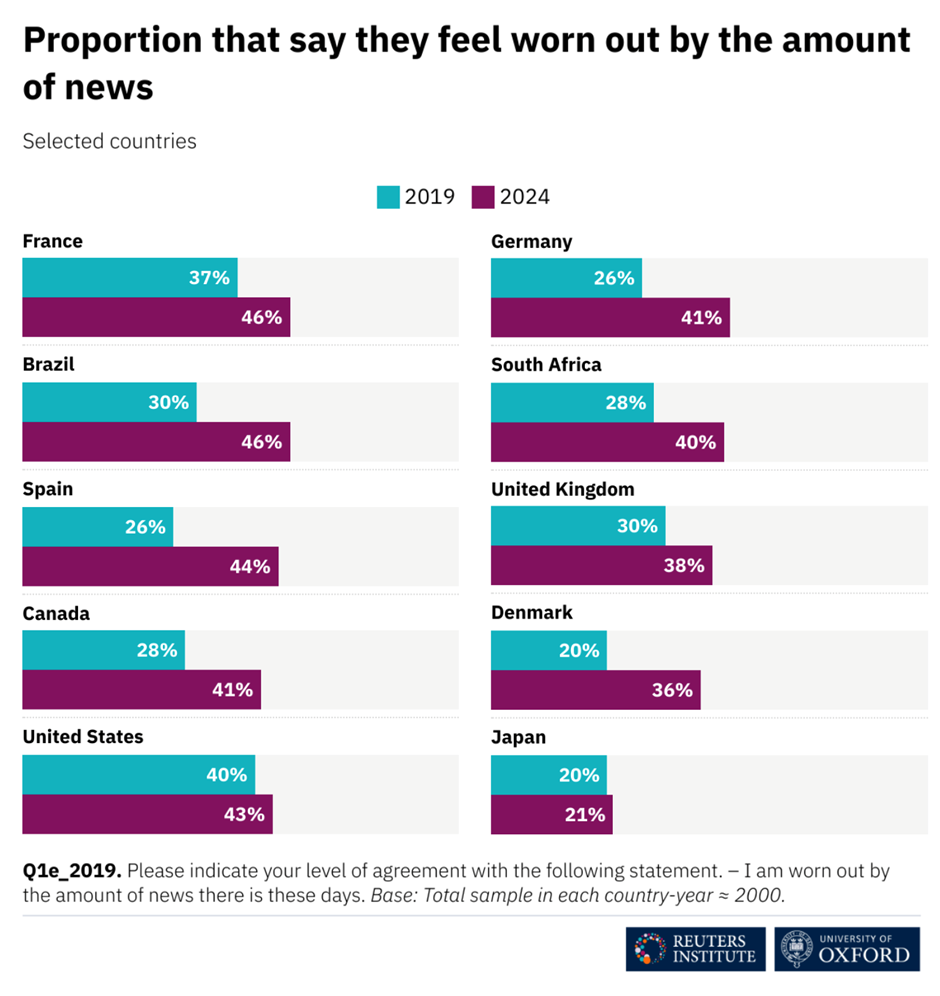

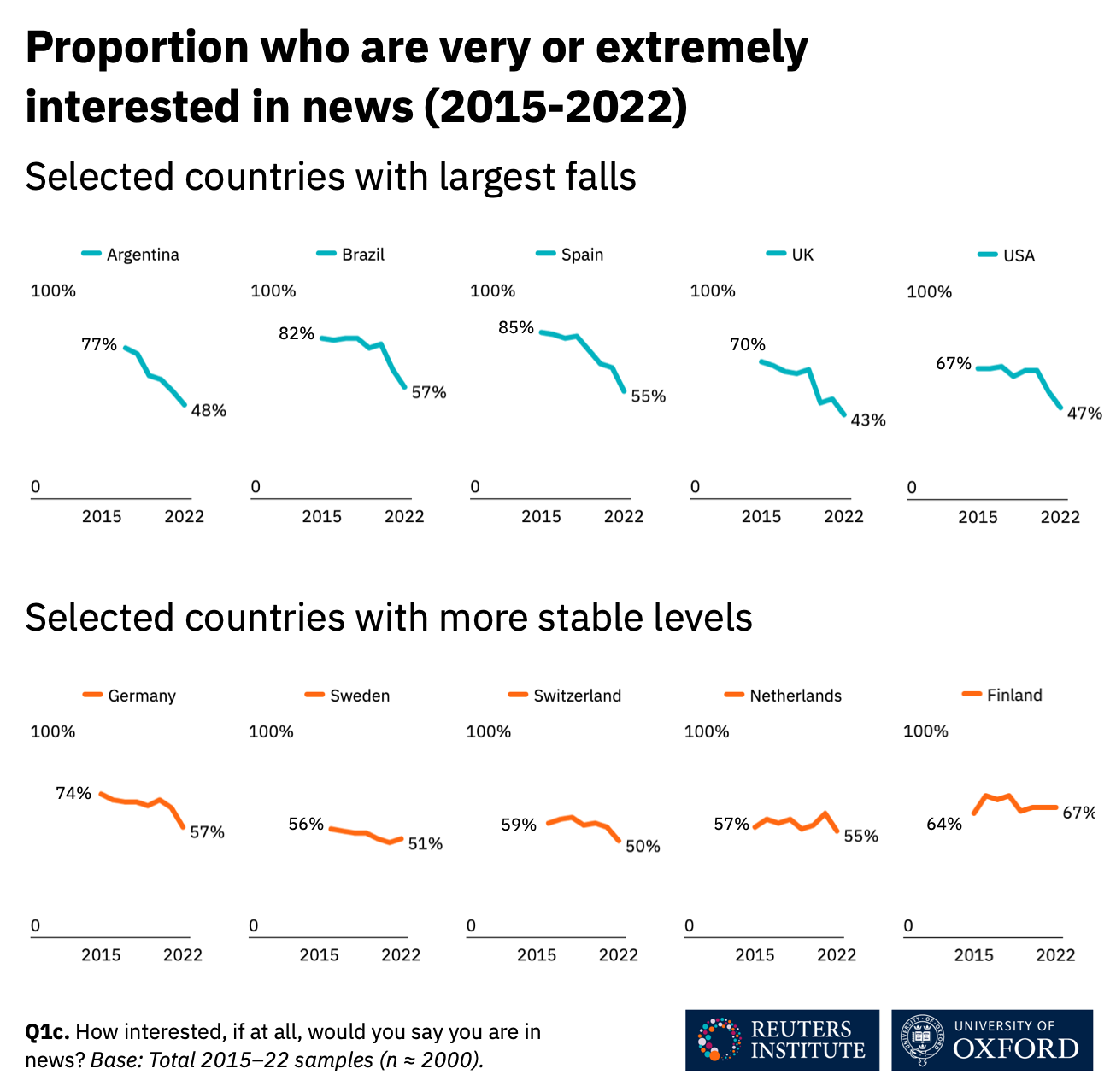

We also document the continually fraying connection between much of the public and much of the news media industry. In many markets, trust is limited, interest in news declining, and news avoidance growing. Many of our respondents say they are worn out by the amount of news, up sharply since we last asked this question in 2019.

We know many publishers care deeply about trust in news, and in a more challenging media environment where much of the public, in many cases especially less privileged people, do not trust the news, publishers able to earn and maintain trust may be able to stand out.

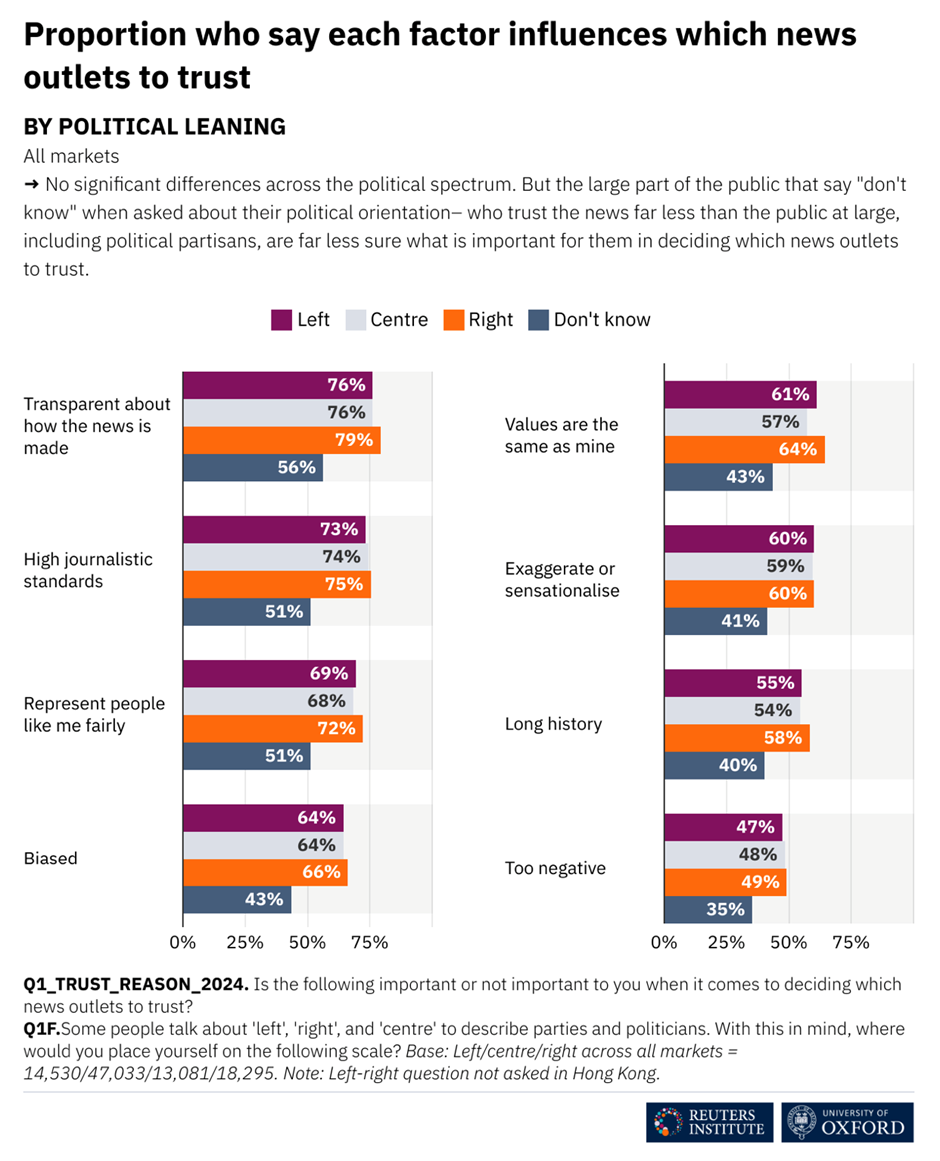

In terms of what factors are important when deciding which news outlets to trust, we show that while people come to different conclusions RE individual brands, across the political spectrum from left to right, most actually emphasize the same factors. The main difference here is not by political orientation but what political scientists call “the other divide” – the large group of people who are more distant from conventional politics (and often less privileged in terms of income and education) are less sure what, if anything, would lead them to trust a news outlet.

That and much more in the full report, which is freely available here.

I’ve been a migrant abroad most of my adult life but have always thought of myself as Danish, and in today’s world, it is a special privilege to be from a county one can, and can happily, return to.

I will continue to collaborate directly with colleagues at the Reuters Institute at the University of Oxford on projects on AI, the Digital News Report, and Leadership Development as a Senior Research Associate.

It is a privilege to join a strong multidisciplinary department at the University of Copenhagen with colleagues from communication, media studies, CS, and more, and to move to a world-class public university committed to basic research, solutions-oriented work, and life-long learning.

It has been an honour to serve the Reuters Institute community as Director. I know the Institute will go on to greater things with a strong team, a record of independent research, a diverse range of funders, and deep connections with journalists, editors, and researchers worldwide. I’m glad I’ll still be part of that journey even as I start a new one with a focus on working with new colleagues in Copenhagen.

In a new Reuters Institute report, Richard Fletcher and I present an analysis of survey data from six countries.

Many of our respondents are optimistic that generative AI will make their personal lives better, views on whether it will make society better varies more, and when we look across different sectors, while people generally believe generative AI will have a large impact on almost every sector, many distrust that news media and (especially) social media companies will use generative AI responsibly.

This and more in the full report, which you can read here.

A privilege to host New York Times publisher A. G. Sulzberger, who gave the 2024 Reuters Memorial Lecture March 4. Among many favourite lines from his talk is this – “Journalistic independence demands a willingness to follow the facts, even when they lead you away from what you assumed would be true. A willingness to engage at once empathetically and sceptically with a wide variety of people and perspectives. An insistence on reflecting the world as it is, not as you wish it to be. A posture of curiosity rather than conviction, of humility rather than righteousness.”

And an honour to chair the subsequent panel discussion with him, Zaffar Abbas from Dawn, Melissa Bell former publisher of Vox, and Alessandra Galloni from Reuters, all of them people I deeply admire for their work and how they do it.

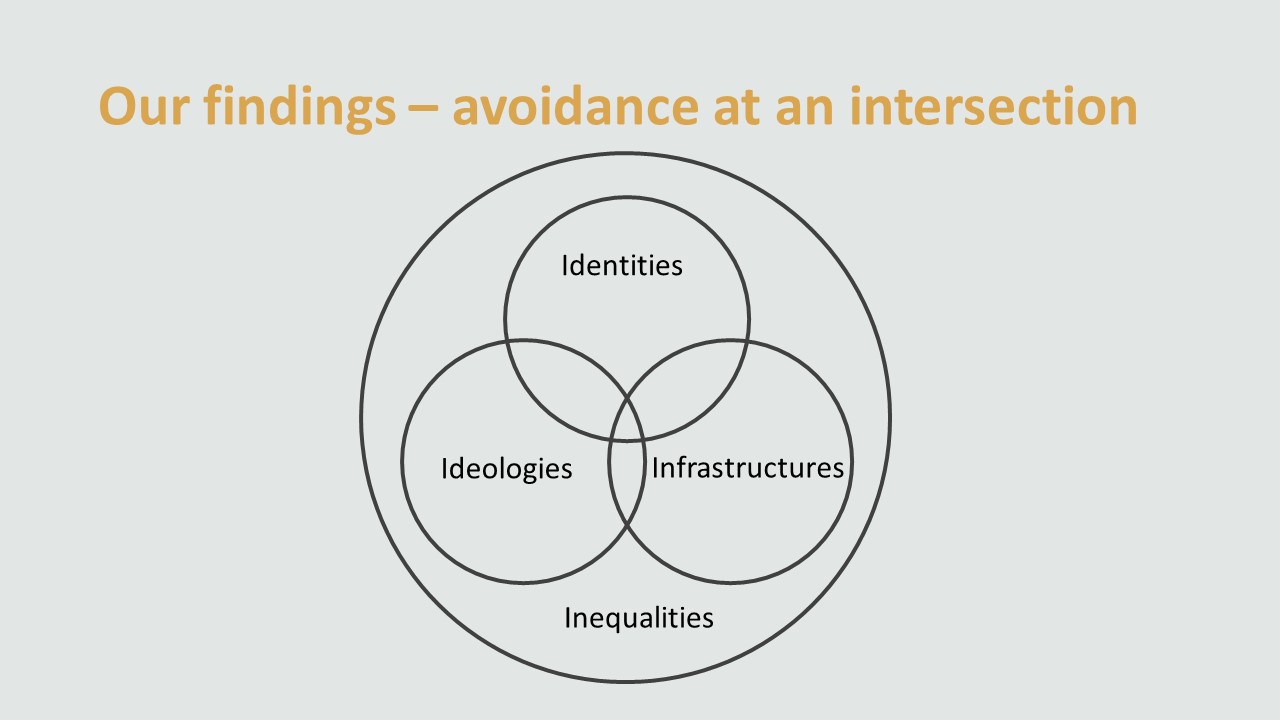

The social contract between journalism and much of the public is fraying – news use is declining, interest in news down, avoidance widespread. Based on survey data and especially well over a hundred interviews with consistent news avoiders, we look at why, and what it means when people live largely without news

We show that news avoidance is not “just” a response to the content on offer. It is also fundamentally shaped by who we are, what we believe, and the tools we rely on.

It happens at the intersection between identity, ideology, and infrastructures, and compound inequalities.

News avoiders, as we explain in the book, and this excerpt from it, tend to be younger, women, and from lower socioeconomic classes. Politics matters too, but this is less about whether people are left- or right-wing and more about the “other divide” between the connected and the disconnected.

In contrast to news lovers (and many regular users), news avoiders tended to see following news as an atomized, solitary activity – they are not embedded in any news communities encouraging regular use. They also often see news as being “not for people like them”, and more for elites.

News avoiders’ conviction that they cannot make a difference politically – and that news certainly will not help them do so – is the core of how they talk about their relationship with news. Whereas news lovers have a sense of political efficacy, news avoiders often do not.

We think avoidance is a problem for journalism, for society, and for people missing out.

But many news avoiders do not see their (distant) relationship to news as a problem. They do not see news as worthwhile, serving people like them, net good for society, let alone a duty.

Because news avoidance is only in part about content, the response cannot be more of the same.

Anyone who wants to respond to news avoidance need to meet people where they are.

“From news for the few and the powerful, to news for all the people.” That is how Juan González and Joseph Torres in their book describe the historical “grand arc of the American press.” That is not the direction of travel now. If anything it is going in the opposite direction.

Whether or not journalists and editors want to do this (in an already difficult and challenging situation) is their decision. For those who do want to address news avoidance, we present five ideas based on our research in the book and in this article.

I wrote a piece for the Financial Times about why I think we need to focus squarely on this as we head into a big election year.

My (naively unworkable) working title when I submitted it was “It’s the elite, stupid: stop gaslighting the public about where consequential misinformation comes from”.

A few links below to evidence that has informed my view.

Third, to state the obvious, some politicians sometimes weaponize false and misleading information for their own purposes. It’s easy to pin this on “populists” – there may be something to this – but it can come from establishment types too – Blair, Bush, Kennedy, Reagan, etc.

Fifth, we don’t need to “forget” technology, as the FT headline suggests, but look at root causes – how political elites make use of tech, and how tech companies react to this use, sometimes treating them differently as a matter of policy, sometimes perhaps for pragmatic reasons.

In summary – misinformation often comes from the top, elite cues are more consequential than more misinformation added to what is already a vast ocean of content, populists may be particularly likely to use this for political purposes but they are not alone, and some politicians want to be allowed to act as they please. There is a lot of research on misinformation – if you are interested in more, great and warmly recommended resources include the “Critical Disinformation Studies” syllabus from CITAP, Brendan Nyhan’s “Political Misinformation” syllabus as well as (both of these are pretty US-focused) for example the edited volume “Disinformation in the Global South” for a wider view.

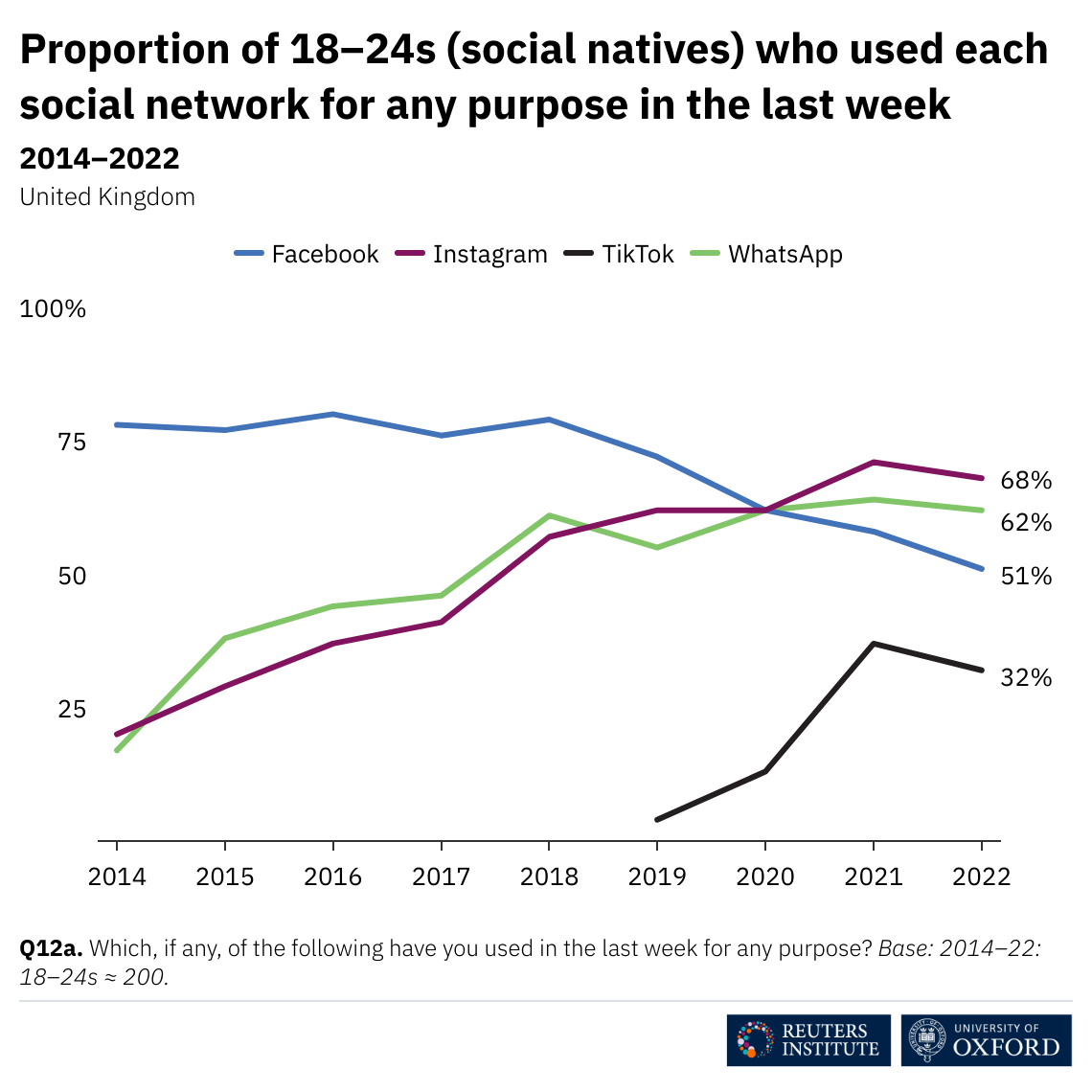

We document how many coming of age now eschew direct discovery for most brands, have little interest in conventional news offers oriented to older generations’ habits, interests, and values, instead embrace participatory, personable, personalised options offered via platforms.

This shift in media use is accompanied by ‘generalised scepticism’, not just low trust in news found via social and search (as we have shown before) but also concern over whether online news is real or fake (esp. among those who say they mainly use social media as source of news).

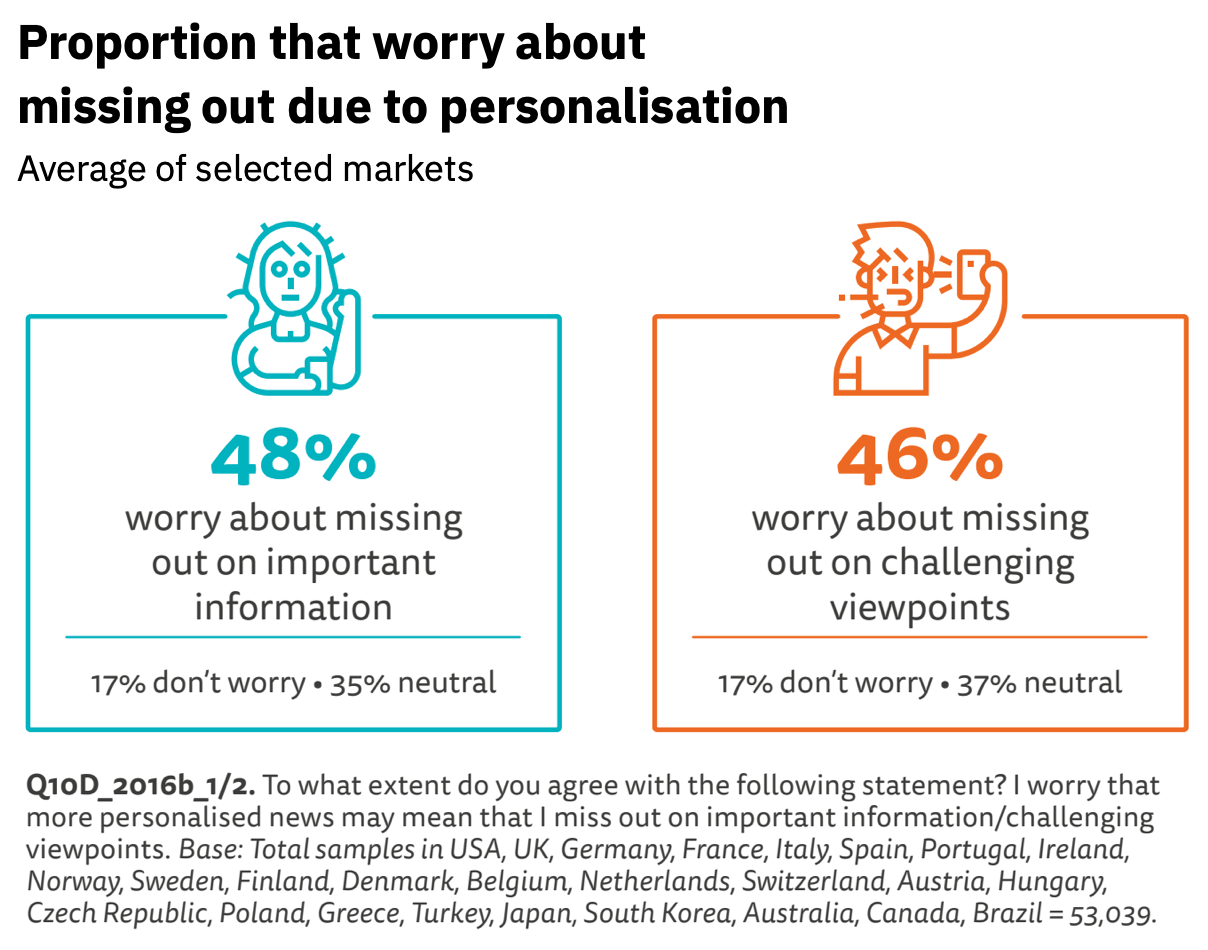

And there are other concerns around platforms and algorithms – across the countries where we asked, nearly half agree of respondents ‘worry that more personalised news may mean that I miss out on important information’ (48%) and ‘miss out on challenging viewpoints’ (46%).

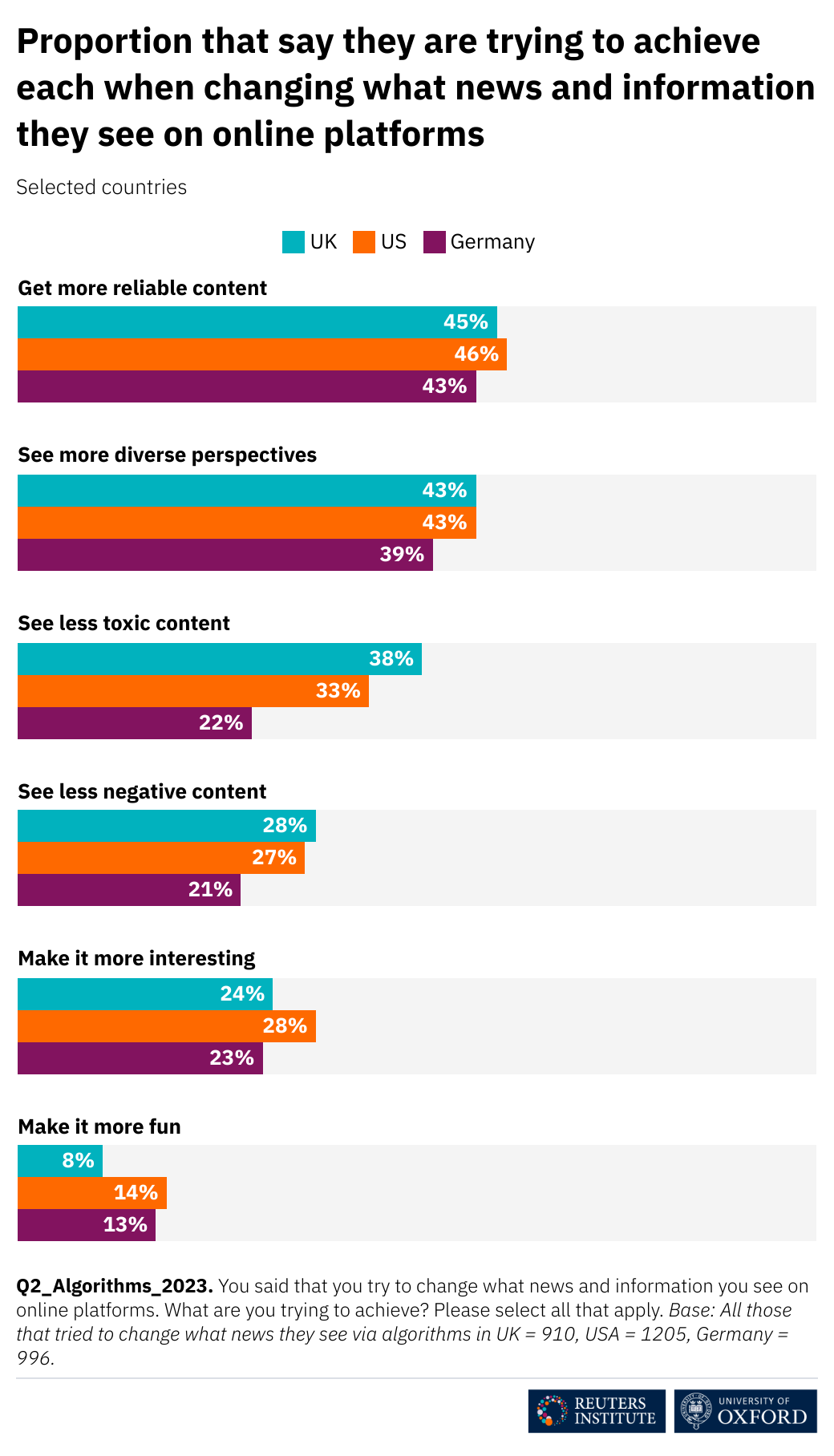

Active online participation with news is declining (offline too), and concerned about what they see on platforms, majority of respondents say they have tried to influence story selection in one or more ways (e.g. changing settings), with different objectives (and rarely more fun).

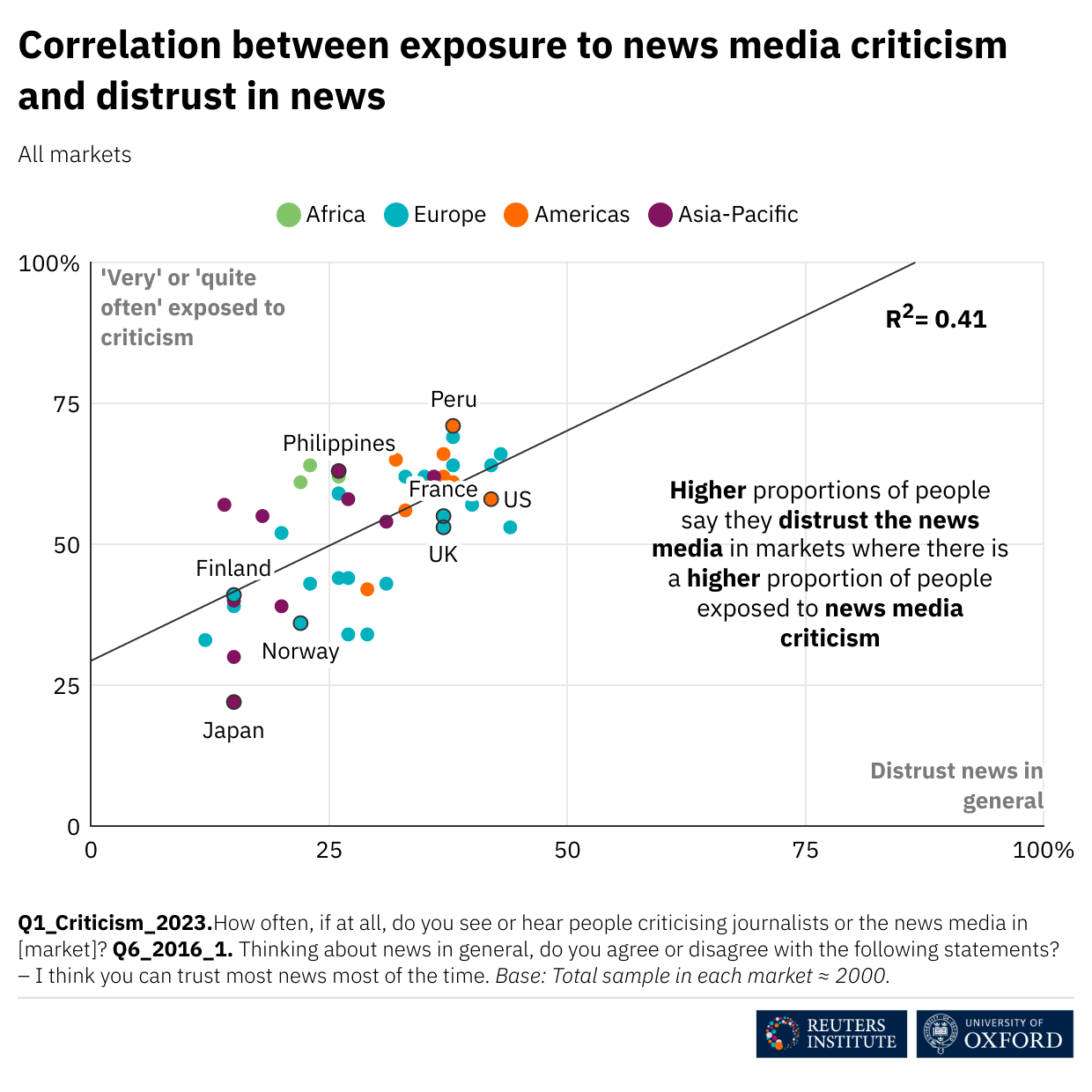

Social media platforms is also where respondents are most likely to say they come across people criticising journalists or the news media. These criticism are often driven by politicians, and looking across our dataset, we find a correlation between exposure to media criticism and low trust in news.

Despite reservations over misinformation, trust, algorithms, and more, the “new normal” is a world where people overwhelmingly, everywhere, opt for digital media in terms of their use – and are often not paying attention to mainstream outlets and journalists even when it comes to news.

This is a super difficult environment for the business of news. On one side, various competing platforms are attracting most online advertising. On the other, many different subscription offers compete with news, and most news subscriptions go to a few winners, mostly upmarket national titles.

Report lead author is Nic Newman, working with Richard Fletcher, Kirsten Eddy, Craig Robertson and myself.

It is made possible by 18 sponsors, our amazing country partners, and the whole Reuters Institute team.

It’s a community effort, and I’m so happy to be part of this community.

We are using the hashtag #DNR22 for discussions on Twitter.

As I write in my foreword, we live in an age of extremes, also when it comes to some aspects of news and media use.

While many of the most commercially successful news media are doing well by primarily serving audiences that are, crudely put, like me – affluent, highly educated, privileged, in many countries predominantly male, middle-aged, and white – questions continue to mount around the connection between journalism and much of the public.

The purpose of our research at the Reuters Institute is to ensure that reporters, editors, and news media executives and others who care about the future of journalism can understand these trends and many others on the basis of reliable, robust, relevant research that can help inform how they – on the basis of their different ideals and interests – chose to adapt to a changing environment.

The Digital News Report is a key part of this.

Seven highlights from this year’s report below.

First, we find that a growing number of news media willing to embrace digital and able to offer distinct journalism in an incredibly competitive marketplace do well by doing good. But many struggle in an unforgiving winner-takes-most online environment, for example when it comes to subscriptions.

Second, while many commercially successful news media primarily serve audiences that are, crudely put, like me (affluent, highly educated, privileged etc) our findings document connection between journalism and much of the public is fraying. Interest and trust is down, news avoidance up.

Third, more broadly, in many countries much of the public question whether the news media are independent of undue political or government influence – even in very privileged countries, barely half say news media are independent of undue influence most of the time.

Fourth, these issues are compounded by differences in how new generations use media – looking specifically at those under 24 we find much less interest in connecting directly with news media, different views on what journalism ought to look like, much heavier reliance on newer forms of social media.

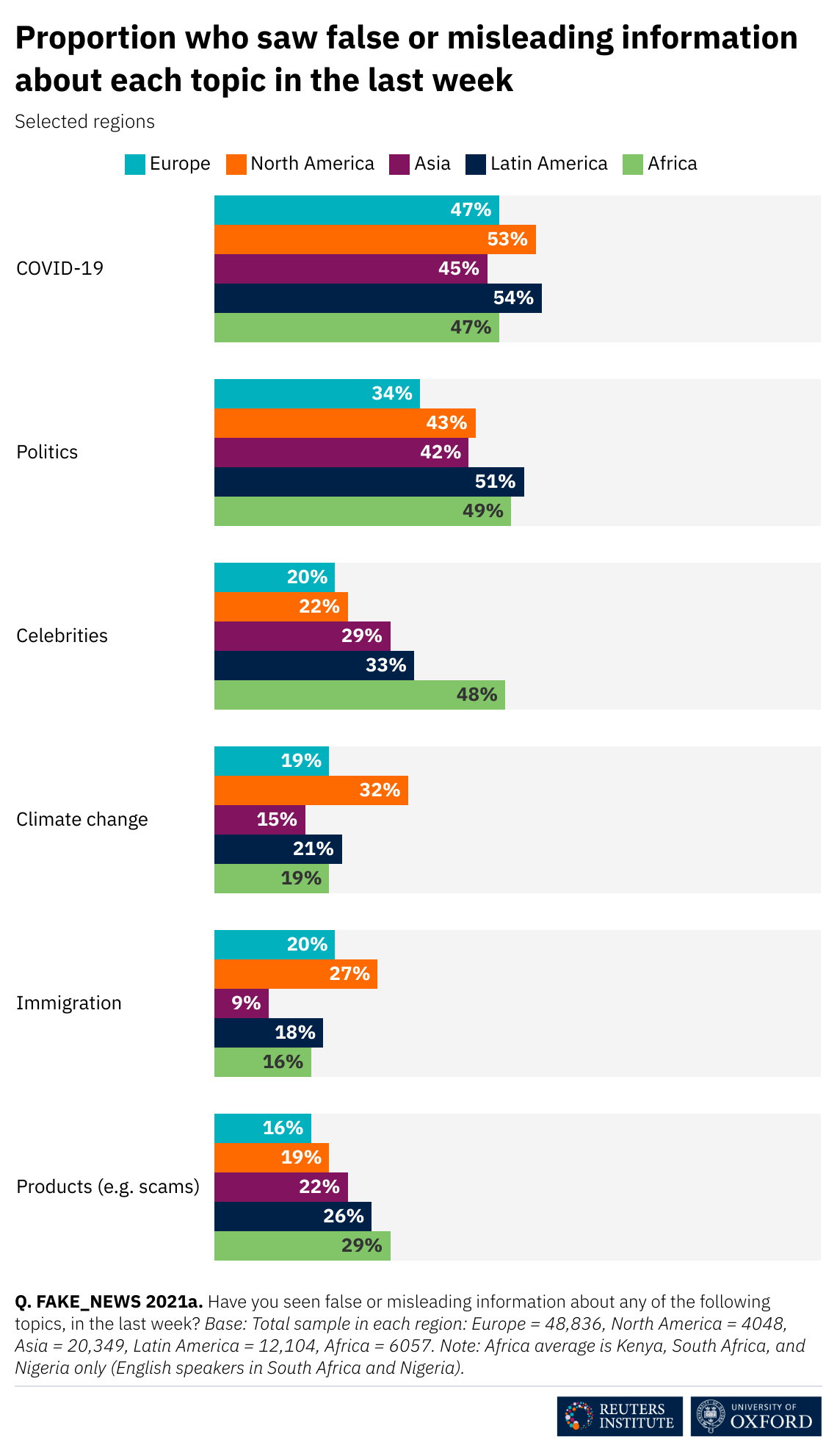

Fifth, across markets 54% say they worry about identifying the difference between what is real and fake on the internet when it comes to online news. More of those who say they mainly use social media as source of news (61%) are worried than among those who don’t use social at all (48%).

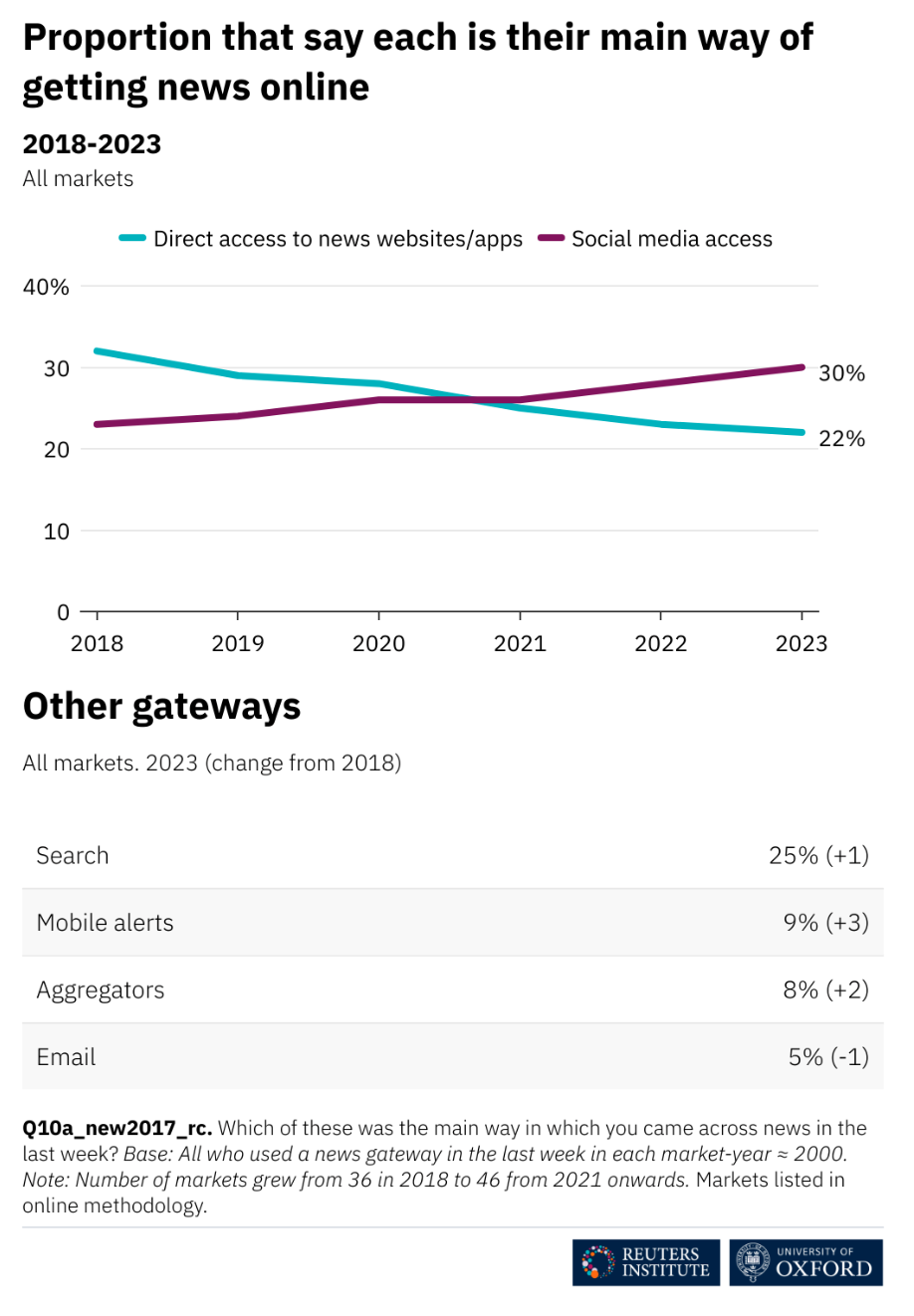

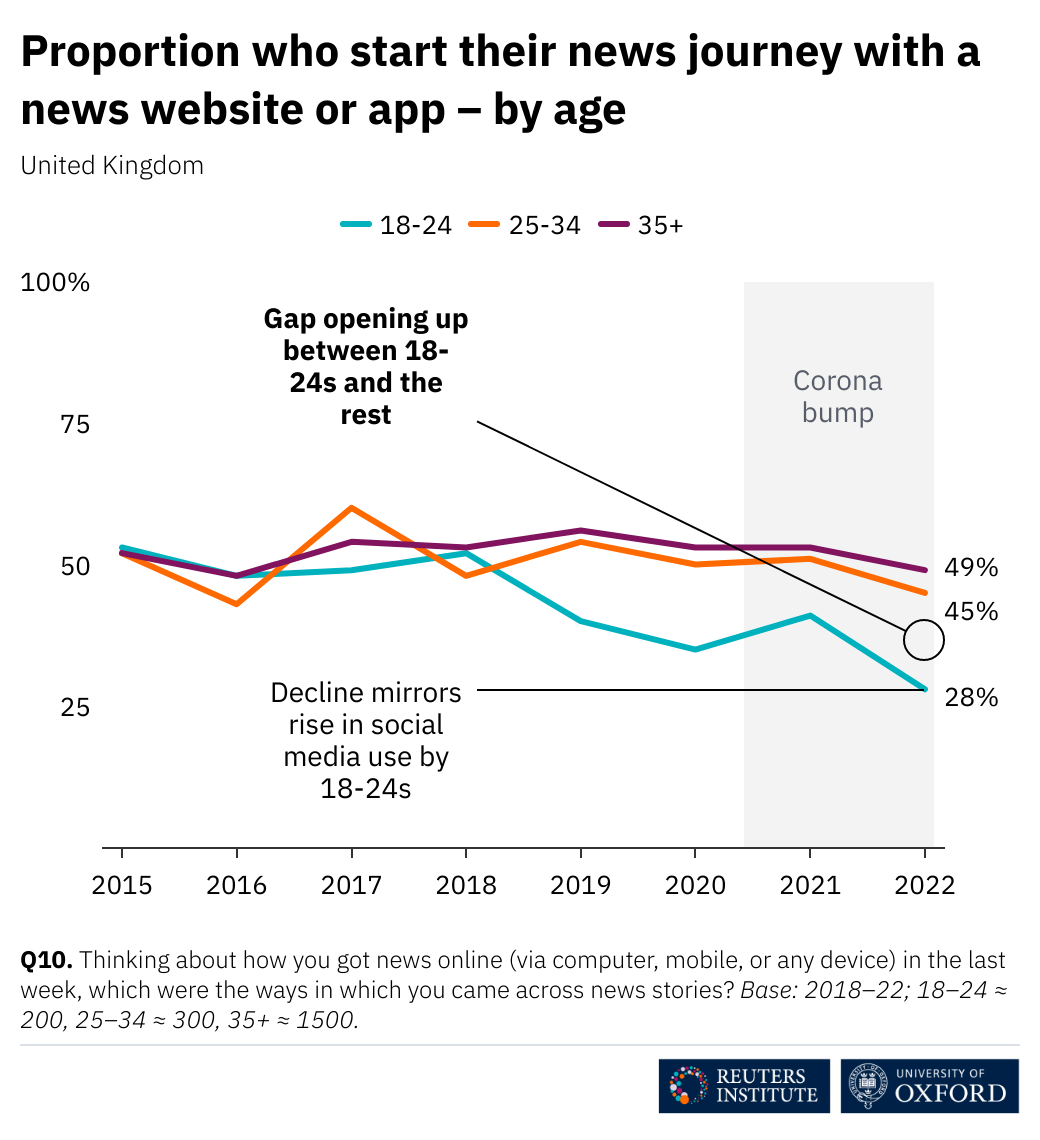

Sixth, despite these concerns, access to news continues to become more distributed. Across all markets, less than a quarter (23%) prefer to start their news journeys with a news site or app, down 9pp since 2018. Those aged 18–24 have an even weaker connection with news sites and apps.

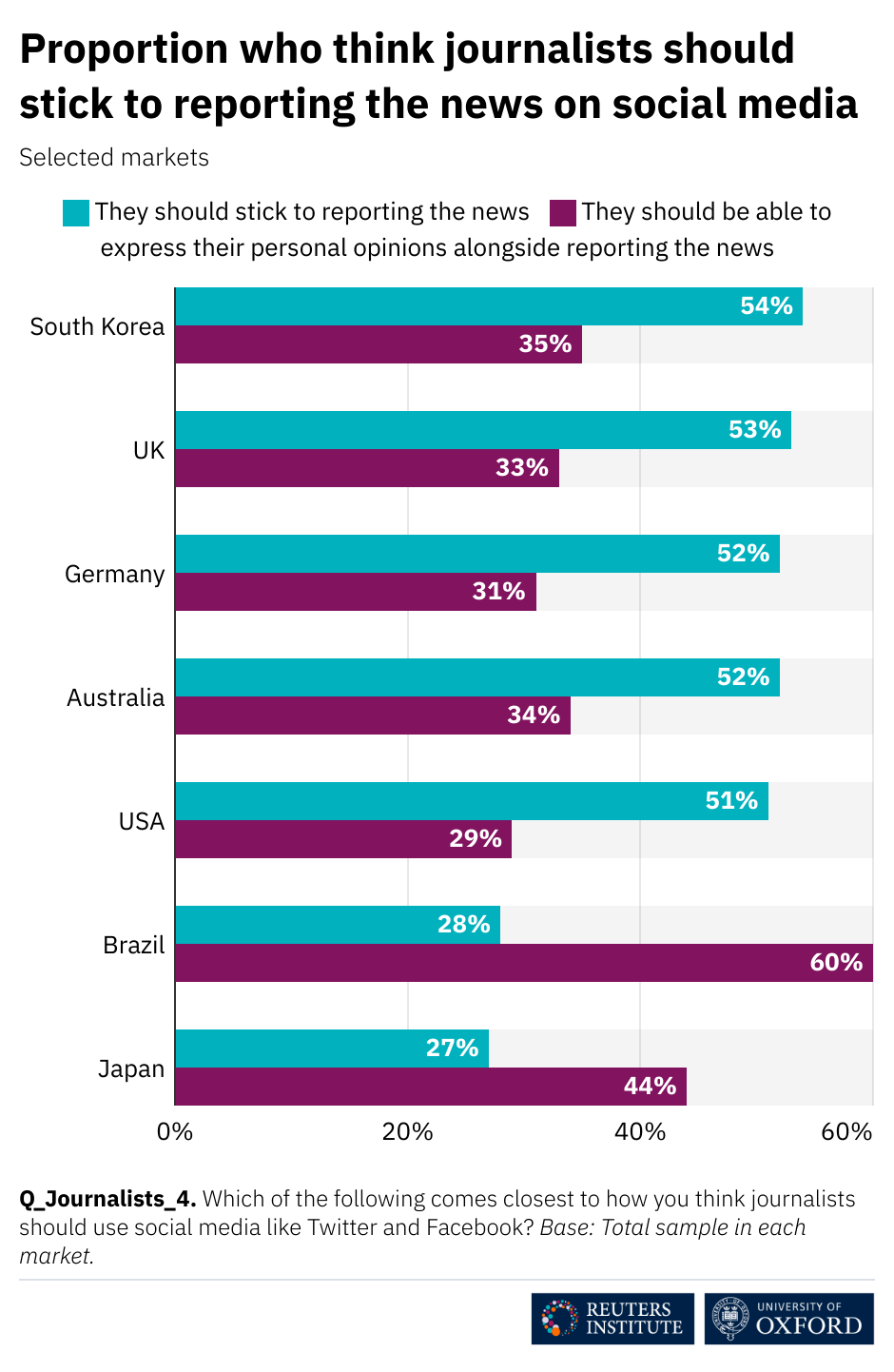

Seventh, as publishers, but also individual journalists, seek to reach people via social media, it is important to note that, in most countries, half or more of respondents feel that journalists on social should stick to reporting the news on social media (even as a sizable minority feel they should be allowed to express personal opinions).

Our core argument is that the power of platforms is deeply relational and based on ability to attract end users and partners like publishers.

It’s always hard to summarize extensive empirical work briefly, but here a few key points from my short Twitter thread on the book, with a few pics of some central passages in the book.

Platforms do not control the means of production, but the means of connection, and they are powerless without partners. To understand their power we need to understand both reservations partners have and why they often embrace platforms nonetheless, continue to work with them.

Platform power is an enabling, transformative, and productive form of power—and power nonetheless, tied to institutional and strategic interests of platform companies, often exercised in highly asymmetric ways.

It goes beyond hard and soft power. We identify five main aspects.

In the short run, actors make choices, in the long run, these choices become structures. Both platforms and partners have agency here, but there is a huge asymmetry between the biggest platforms (facing a few big platform rivals) and a multitude of much smaller publishers.

We approach platform power through an institutionalist lens, and focus on how it is exercised in relational ways through socio-technical systems that develop path-dependency and momentum over time and retain an imprint of their founding logics that shape ongoing interactions.

Our analysis is based on interviews across several countries, observation, background conversations, as well as on-the-record sources and more. In the methods appendix we reflect on individual and institutional positionality, including differences between the Reuters Institute for the Study of Journalism where I work and much of the research was done, and Simon Fraser University where Sarah now works.

The evolving relationships between platforms and publishers speaks to fundamental feature of the contemporary world – that not only individual citizens, but also social and political institutions, are becoming empowered by and dependent on a few private, for-profit companies

Very proud of the advance praise from colleagues with experiencing working in publishing companies, for platforms, as well as some leading academics researching digital media, including from Vivian Schiller, Nick Couldry, and José van Dijck. It means a lot to me personally to read what they kindly had to say about the book in advance of publication!

The research for this book was made possible by the prize money from the 2014 Tietgen Award, which funded Sarah’s position as a postdoctoral research fellow at the Reuters Institute for the Study of Journalism and the associated research costs.

We would like to thank first of all our interviewees and everybody else who has talked to us, joined off-the-record discussions we hosted, invited us to events, and let us sit in on meetings. The book would not have been possible without them sharing their perspectives, and whether they agree with our analysis or not, we hope they recognize the processes they are part of in what we write about here.

In addition, many different colleagues and friends have provided generous (and often challenging!) feedback as we worked on this, including David Levy, the former Director of the Reuters Institute for the Study of Journalism, and our many good colleagues there. Special thanks go to Chris Anderson, Gina Neff, Joy Jenkins, and Lucas Graves, who went through an entire draft manuscript with us and provided invaluable input. Daniel Kreiss and the anonymous reviewer helped further sharpen our thinking, and the series editor Andrew Chadwick went above and beyond in helping us develop our ideas. Fay Clarke, Felix Simon, and Gemma Walsh all did an outstanding job as research assistants at various stages of the project. Angela Chnapko at Oxford University Press masterfully guided us through the publication process.

My presentation notes for opening part of OECD panel on “Competition, Media and Digital Platforms” at the 2022 Open Competition day. Video of whole session here. More context at the end of the post.

News media used to operate in a low-choice environment where they had high market power over both audiences and advertisers.

Before the move to a digital, mobile, and platform dominated media environment, news media used to control both the channels of distribution and bundled the content people accessed, and captured a significant share of both audience attention and advertising spending because of the positions they occupied.

As a consequence, in markets that were geographically differentiated due to how print and broadcast distribution works, a significant number of news media made quite a lot of money by dominating local markets and specific audience niches.

News media now operate in what is, for citizens, a high-choice environment when it comes to content, and have very limited market power over both audiences and advertisers.

In a digital, mobile, and platform-dominated media environment, platforms increasingly control the channels of distribution, news is unbundled and competes for attention with all sorts of other content, and news media capture a much smaller share of audience attention and, as a consequence, of advertising spending.

This is a much, much more competitive market, and one characterized by very strong winner-takes-most dynamics where a few winners are doing well but many titles, especially legacy but also new entrants, have a much harder time making money.

A few key datapoints illustrate this –

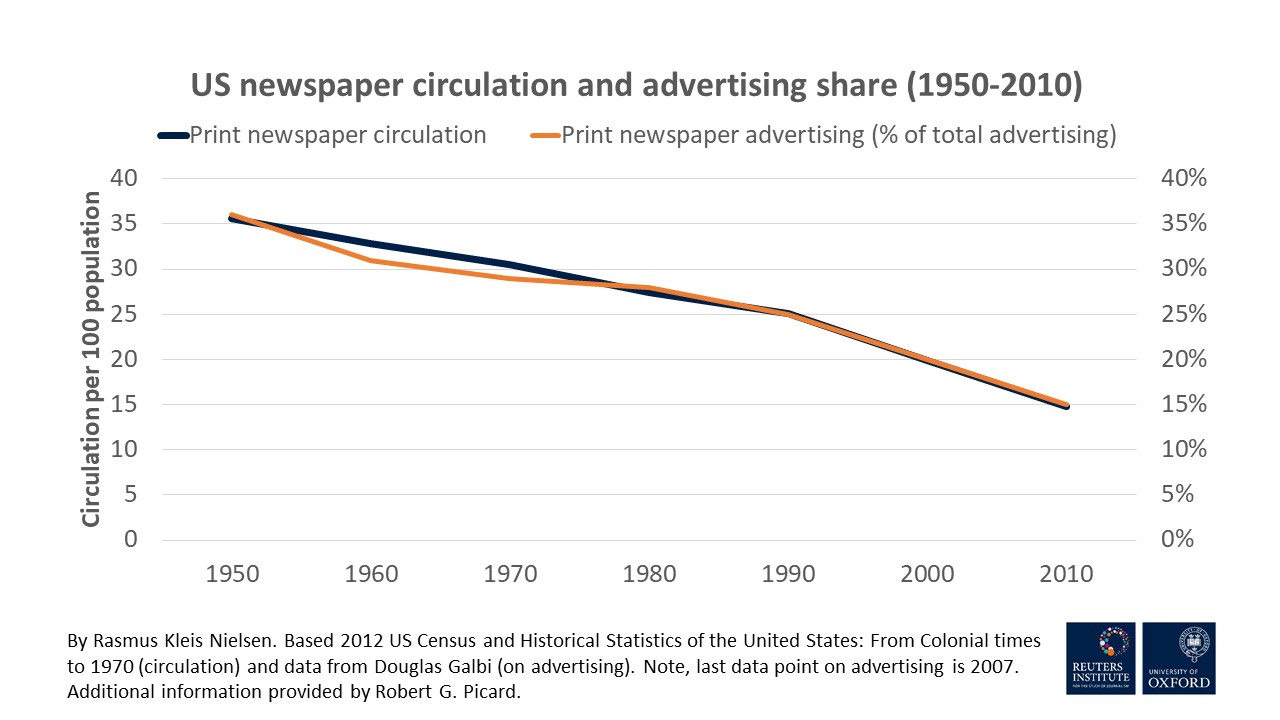

A rough estimate is that people spend something like twenty percent of the time they spend reading print reading news, and something like ten percent of the time they spent watching television watching news.

By contrast, in the countries where we have data, all news media combined account for something like three to four percent of the time that people spend with digital media.

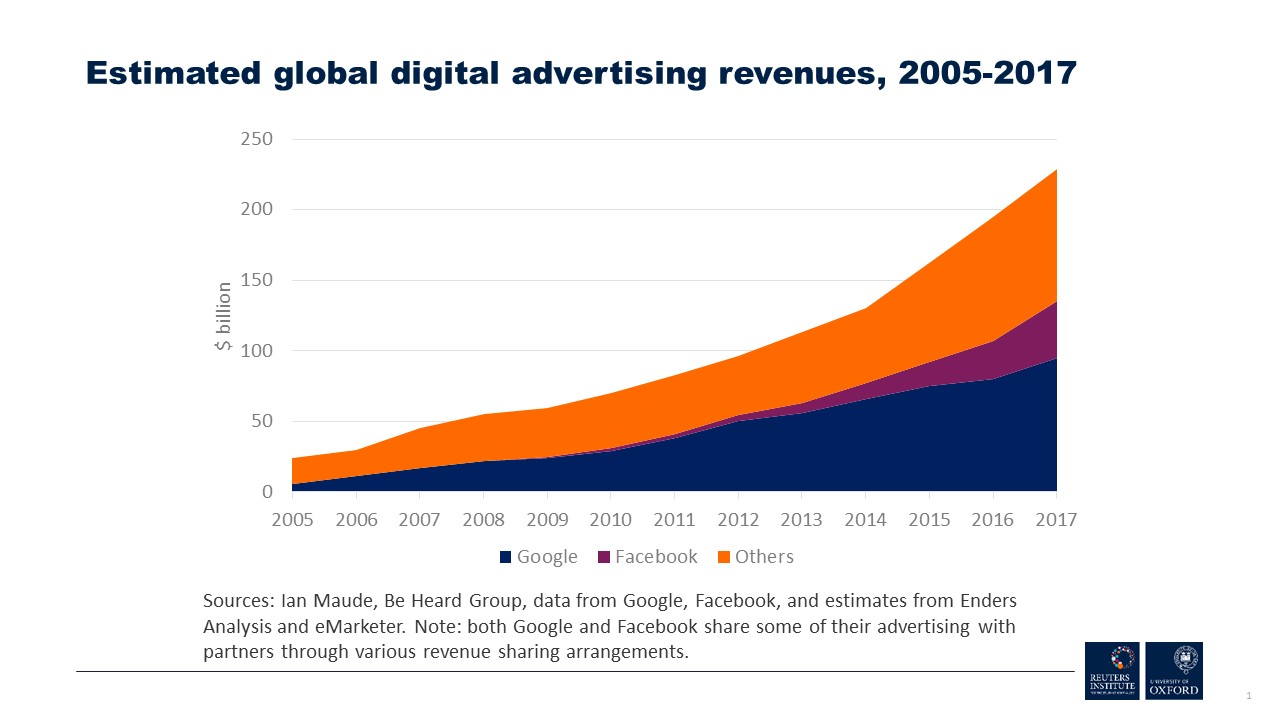

Since advertisers were never interested in the news per se, but in reaching audiences, it is not surprising that they have gone where the audience is.

Online, that is, to a large extend, on platforms – and the popular success and evident market power of a few big platforms, most prominently Google and Facebook, has undoubtedly exacerbated the commercial challenges news media face as they account for a large share of total advertising sales.

The biggest platforms are the face of the challenge, but they are not all of it – it is important to recognize that, according to eMarketer, globally, most of the biggest sellers of digital advertising are platforms who can offer very low prices, very detailed targeting, and often both depth and breadth in terms of audience reach.

Advertisers still spend some money with news media, especially those news media who can offer premium brands and an advertising environment that stands out from just “stuff on the internet”. But over time I’d expect the share of advertising spending that goes to news media won’t be much higher than the share of audience attention that goes to news media – and, as said, right now, that’s a few percent.

If we look at those few percent of attention, and the news media industry specifically, we can see that the shift from a pre-digital to a digital environment has further intensified existing winner-takes-most dynamics.

In the past, economies of scale and high barriers to entry drove consolidation and the formation of local monopolies and oligopolies. Media markets have always been highly concentrated.

In a digital environment where geography no longer presents a meaningful barrier to entry, the same dynamics are playing out at a national level and to a smaller extend at a global level.

Look at attention, and by extension advertising, first.

In the markets where we have data, out of hundreds of competing news media, typically, a handful of titles – almost always national brands – account for half or more of all time spent with news online.

That’s the big head – at the long-tail end of the distribution, in the US, all local news titles combined have been estimated to account for less than one-sixth of all time spend with news online, in the UK, about one-tenth.

It stands to reason that a tiny amount of attention combined with no market power over audiences or advertisers is less lucrative than being the dominant player in local content and local advertising.

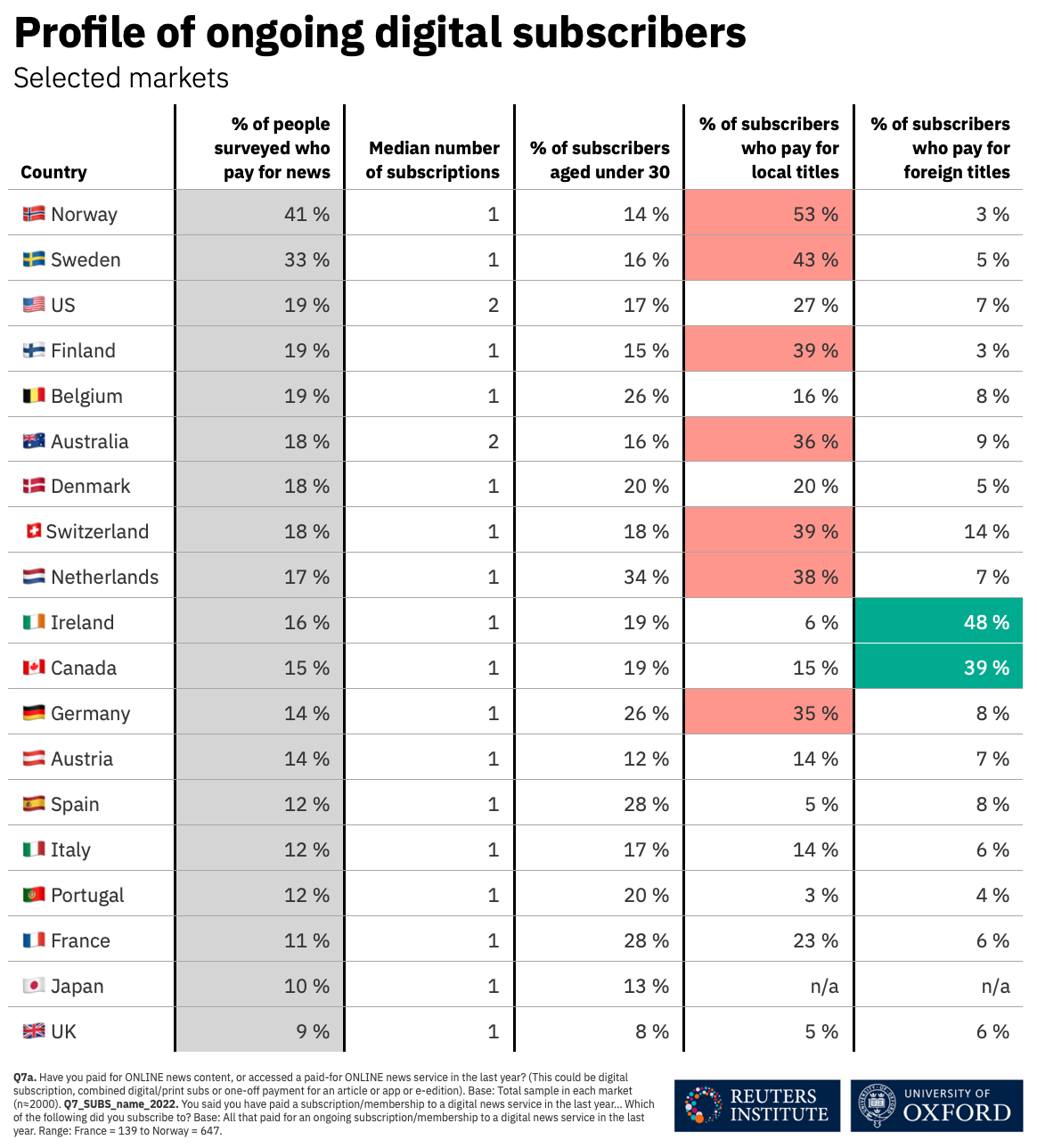

Look at paying for news next.

Here too we see strong winner-takes-most dynamics. In the markets where we have data, again, a small number of predominantly national titles, out of hundreds of news media, often account for half or more of all digital news subscriptions.

They are the big head – at the long-tail end of the distribution, with some important exceptions, local titles have seen limited growth in digital subscriptions.

Where does this leave us?

It leaves us in a place where I think we should expect top-line revenues in the news industry as a whole to continue to decline for some time, driven primarily by audience and advertiser choices, and compounded by the success of platforms, as relatively lucrative legacy print and broadcast operations continue their long-term structural decline (print, traditional TV) or at best stagnate (which I consider best case scenario for linear scheduled TV) and digital is a much more challenging and competitive market.

And it points to a future where existing winner-takes-most dynamics in the business of news, for both attention, advertising, and reader revenues, are reinforced.

It will probably be a smaller industry than news was in the 1990s – but with a few percent of total advertising expenditures, a growing number of digital subscribers served at near-zero marginal costs, and auxiliary revenues from ecommerce and the like it will still be a multi-billion dollar industry, and one that will probably invest a greater share of revenues in editorial than it ever did, because the very high distribution and production costs associated with offline are falling away.

Compared to the recent past, it will be characterized by few winners – dominant national titles, and those new entrants who make good use of the gift of digital distribution at low cost, keep their content distinct and their costs low, and manage platform risk well.

And there will be many losers – especially among also-ran national titles, local titles stuck with a pre-digital cost structure, as well as titles trying to build a sustainable business around serving less privileged and often historically underserved parts of the public (as well as all titles with owners who prefer short-term asset stripping over the uncertain returns on long-term investment in digital transformation).

It’s going to be amazing for people like me, the most lucrative affluent, highly educated, news loving part of the public. It’s looking a lot more mixed for the majority of the public. The latter point is potentially problematic if one believes, as I personally do, that independent professional journalism, with its imperfections, play an important role in our societies, but that is more a political question.

As part of the opening, I was given four minutes to say a few things about the following questions: “How has news media changed in the digital age? Changes in the revenue model and changes in consumer behaviour? Any difference between large and small/local outlets?”

This post contains my presentation notes – a lot of ground to cover in four minutes! They draw on this handbook chapter from 2020, which I still hope is useful in capturing the main dynamics as I see them. I’ve added a few links to underlying evidence and two charts taken from the handbook chapter.

Two addendums to the notes above. First, as I made clear in the panel discussion, OECD member countries are very different, and so is the business of news (and political context) from case to case, this is just an attempt to capture what I see as the high level trends. Second, in the panel I somehow came to be cast as the pessimist – that’s not how I personally think of my analysis. While sobering, I think it also gives ground for evidence-based optimism. Whether you find it optimistic, pessimistic, or realistic, I give it in the spirit of James Baldwin’s piercing line: “Not everything that is faced can be changed; but nothing can be changed until it is faced”, hence the title of this post.

(Oh, and finally, I wonder how many other presenters at OECD events are caught red-handed on video with a half-dozen Foucault books on the shelf behind them!)